People who forget to go on mute during conference calls

How slowly the clock ticks towards 5 o’clock on a Friday afternoon

Randy from accounting

Stacks and stacks of TPS reports

If you’re waving your fingers and toes in the air now, you might find this lesson rather interesting.

Retirement may seem like a hazy dot far off on the horizon, or simply an impossibility. However, with some careful planning and laser-like focus on the goal, you can get there. Things that are not required (although they sure help): A six-figure salary; a whopping inheritance; a lucky lottery ticket.

In this lesson we’ll take a look at a couple of inspiring stories of people who managed to leave behind the rat race at stunningly early ages. We’ll also discuss how you can shape up a plan to do the same.

Off The Beaten Track

If you haven’t heard of Mr. Money Mustache (MMM), I am pleased to introduce you. MMM and his wife earned normal salaries, managed to save the vast majority of their paychecks through frugal living, invested wisely in index funds, and here’s the good part — they retired at the ripe old age of 30.

The MMM family can now be found stomping around Longmont, Colorado with their son in tow. They’ve left the working world for good.

If you’re ready to fall down the early retirement rabbit hole, read through:

If you’re tempted to ditch this course for an hour or two of binge reading, I won’t blame you. I’ll wait right here…

When I first stumbled onto MMM’s website, I simply couldn’t stop reading. Article after article challenged the conventional wisdom that I thought was true:

Get a good job — stick with it for decades — if you play your cards right, when you’re 65 you’ll be able to put your feet up and call it quits

You need millions of dollars in the bank to retire

A purposeful life is gained one promotion and corporate accolade at a time

If you want to work until you’re 65, climb up to the highest rung of the corporate ladder, save up your millions, these are perfectly valid choices. These choices aren’t better or worse than others.

But, the fact is that these ARE choices.

This was the light bulb moment for me: you don’t have to follow the standard life path if you don’t want to. There are other ways to live your life. You can gain freedom before you go gray.

Not to be outdone, another incredible story comes from Justin at the blog Root of Good. He and his wife live in Raleigh, North Carolina with their three children. Justin retired at the age of 33. For a blow-by-blow account of how they made it happen (filled with great tips and nitty gritty detail), check out:

While you’re still many years away from retirement, there’s no use in modelling out a fine-tuned plan for how much money you need. Too many variables will change in the future for this to be a worthwhile exercise.

Pick a “north star” that you can work towards. I recommend you set your initial “retirement number” at an investment portfolio that is worth your expected annual expenses in retirement, multiplied by 25 to 30.

There are two parts to this simple equation:

Your expected annual expenses in retirement, which should be based on your current spending habits, with adjustments made for lifestyle changes that you expect to have in retirement (More travelling? Kids will have moved out of the house?)

A multiplier of 25 to 30. The higher the multiplier number you choose, the less chance you’ll have of running out of money in retirement, but the more money you’ll need to save up to meet your goal. Note that this corresponds to a “withdrawal rate” of 4% to 3.33%

For example, if you expect your expenses to be $50,000 per year in retirement, your target retirement goal should be to save up an investment portfolio worth $1.25M (25 times) to $1.5M (30 times).

To make your initial planning super simple, use this retirement date forecasting spreadsheet. After you input your assumptions, it’ll tell you how much money you need, when you’ll get there, and will show you a few what-if scenarios as well.

Go with this simple estimate for now. As you get closer to your goal, you can start to tweak the numbers. You’ll have a better idea of what your expenses in retirement actually will be. You’ll also know the amount of any pensions or social security payments that you’ll receive.

Conclusion

There’s nothing wrong with wanting to follow the standard path of retiring at 65. But, if that’s not for you, know that there are other ways of designing your life. Retiring in your 30s, 40s, or 50s is achievable with the right mix of planning, dedication, and patience.

To get there:

Set your sights on a retirement number — start with a simple estimate based on your expected annual expenses in retirement multiplied by 25 to 30

Keep chugging along with the same skills that you’ve been building throughout this course: tracking your spending, spending less than you earn, and investing the difference wisely

Tweak your plan as you go along. Sit down at the end of the year to assess where your net worth is, adjust your retirement number as needed, and get back at it

You’ve reached the last lesson in this course. Congratulations!

Before I leave you, here’s a list of the most important points that I hope you take away from this:

Review your finances on a regular basis. Track your net worth and your cash inflows & outflows — once a month is a great rhythm to keep

Always keep an emergency fund on hand, holding at least three months of living expenses. Keep that money in a no-risk and easily accessible account. I recommend a high-interest savings account

Enroll in employer matching programs (read: free money) if they’re available to you

Pay off your entire credit card bill and all other high interest rate debt (5%+) before starting to invest your money

Don’t take risks with money that you need in the next few years; for that, stick to a high-interest savings account

When it comes to investing, start early and make regular contributions — even if its just a small amount every month

Invest your savings in low-cost index funds which track the overall market (couch potato strategy)

Keep your eyes on the long-term horizon, and don’t sell your investments when things look bleak — time in the market beats timing the market. Be patient!

Use tax-sheltered investment accounts as much as possible (read: pay less taxes)

Automate your plan as much as possible. Use auto-deposits to make your plan happen seamlessly and to reduce the risk of busting your budget

A financial plan is not a static thing. Adjust yours as time passes

Building wealth is a marathon, not a sprint; don’t try to turn your life upside down and do everything at once. Take it step by step

Comparison is the thief of joy — the net worth of others is no reflection of your self-worth

Build the life you want, then save for it

So Long… Partner

Thank you for sticking with me ’till the end.

Now that you’ve heard me drone on and on (and on) for 20+ lessons, I’d love to hear from you.

Was this course helpful for you? Was it too short, too long, or just right? How could I improve this guide? For any feedback, random thoughts, or just to say hi, feel free to shoot me an email at themeasureofaplan@gmail.com.

If you’d like to support what I do, you can buy me a coffee or beer by clicking the little blue button below. Any contributions are an immense aid in keeping this site up and running with fresh & free financial content!

P.S. — I’ve included two last posts in this series. The first has a few book recommendations, and the second has some online recommendations. These are fantastic resources to go through if you’d like to continue your personal finance education.

Moonshine Money: A Do-It-Yourself Guide to Personal Finance

Before jumping into discussions about budgeting, saving, and investing, I want to spend some time to make sure that you know how to read your paycheck. After all, we can only save and invest money that we’ve earned in the first place.

In this lesson, we’ll dig into these key concepts:

Gross salary

Taxes

Deductions

Net salary (also known as take-home pay)

Gross Salary

When people talk about their annual salary (e.g., $40,000 per year) or hourly salary ($20 per hour), they are almost always talking about “gross salary”. This is the headline number that appears on your employment contract.

This figure is only a starting point.

Unfortunately, the money that appears in our bank account after each pay day is lower than what our gross salary would suggest. Think of your gross salary as the entire pie. After taking off slices for taxes and deductions (discussed below), the remainder is of the pie is what actually gets deposited into our bank account.

Taxes

It’s morbid but true: ’Tis impossible to be sure of any thing but death and taxes.

When you earn money from your job, your employer will automatically subtract taxes off of your gross salary (boo). Your employer sends this money to the government on your behalf.

The main form of tax taken off from your paycheck is income tax. The amount of income taxes you pay are based on the concept of “tax brackets”. As your income gets higher, the percentage of your income that you pay in tax increases.

Here’s an overview of income tax brackets for Canadians and for Americans.

Side note #1: It’s a common misconception that you should try to stay below certain income levels, since shifting into a new tax bracket would reduce your overall take-home pay (i.e., higher salary but lower money coming into your bank account at the end of the day). This is absolutely NOT true.

When you move into a higher tax bracket, it’s only the money earned within that new bracket which is taxed a the higher rate, not your entire salary.

Side note #2: The taxes taken off your paycheck are a “withholding” tax, meaning that they are just an estimate of the amount that you should owe. At the end of the year, the actual amount of taxes that you should have paid will be calculated on your tax return. The resulting difference between what you paid and what you should have paid will be settled at that point (either through a tax refund or additional taxes owed).

Keep this in mind if you see something odd happen with your taxes on your paycheck (for example, when you receive a bonus). You will always get “trued-up” at the end of the year.

The bottom line: the higher your income, the more tax you pay. However, making a higher income will always increase the pay that hits your bank account.

Deductions

Depending on what company you work for, you may have other deductions that are taken off of your paycheck. These could include contributions to an employer stock option plan, an employer pension / retirement savings plan, or an employer health plan.

When you were first hired, HR may have given you forms to sign up for an employer retirement savings plan (often known as a “Group RRSP” account in Canada, or a “401k” account in the US). If you signed up, you’d be contributing a portion of your paycheck towards these savings plans (e.g., contributing 2% of each paycheck towards that account).

These amounts are deducted directly from your paycheck. As such, this money never arrives in your bank account. Instead, it’s held separately in a different account.

If this all sounds like mumbo-jumbo, we’ll talk about this in a future lesson on employer matching.

Net Salary (Take-Home Pay)

Gross salary is the full pie that we start with. After taking off a slice for taxes, and another slice for deductions, the amount of the pie remaining is what’s known as net pay or take-home pay. This is the amount of money that actually gets deposited into your bank account.

Your take-home pay is the most important number for you to know, since ultimately this is the money that you have control over. This is the money that pays the bills or gets saved for the future.

Knowing the amount of money that you take home each month will serve as a key input for the financial plan that you’ll build throughout this course.

An Illustrative Example

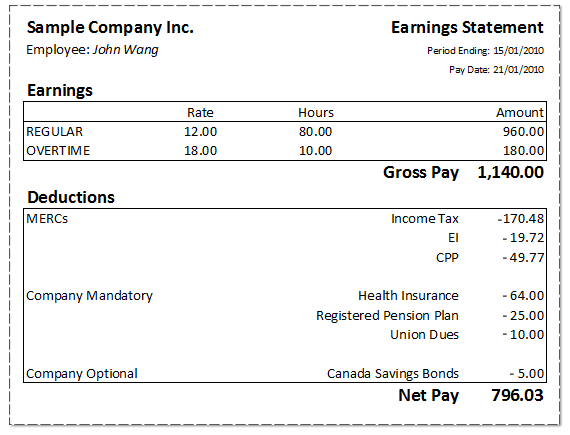

Let’s take an example from a hypothetical Canadian paycheck:

For these two weeks, John earned a gross salary of $1,140 (regular pay plus overtime pay)

John paid total taxes of $239.97. This consisted of income tax, employment insurance (EI), and Canada Pension Plan (CPP) payments

John also had deductions of $104 for health insurance, registered pension plan, union dues, and Canada savings bonds

As a result, John had take-home pay of $796.03 for these two weeks ($1,140 minus taxes of $239.97 and minus deductions of $104)

John’s average tax rate was 21% for this paycheck (total taxes of $239.97 divided by gross pay of $1,140)

Note: The American version of CPP is known as Social Security.

Your Assignment

Open up your latest paycheck (these may be mailed to you, or available for download from your company’s internal website)

Similar to the example above, calculate your gross pay, taxes, deductions, and take-home pay (remember: take-home pay is equal to gross pay minus taxes and minus deductions)

Calculate your average tax rate (also known as effective tax rate). To do this, divide the amount of taxes you paid into your gross pay amount

Resources

To get a quick and dirty estimate of what your take-home pay would be at different gross salary levels, try out these tools below. These can come in handy for estimating what your take-home pay would be after a raise, when moving to a new job, or just to perform what-if analyses.

Unfortunate events happen. They’re not fun to talk about, think about, or imagine; but they happen. Burying your head in the sand won’t change that reality. Having the appropriate insurance can help you and your family stay afloat during these tough times.

Insurance plays an important role in your “financial armor”. Your emergency fund will help you to weather relatively small or short-term issues, but insurance is the thick inner layer of defense against more serious or long-term events.

For those who have others depending on your income — children, elderly parents, or a spouse who doesn’t work, insurance becomes all the more critical.

Even if your income is solely used to support yourself, if injury forces you to leave the workforce, the impact on your savings could be significant.

Find Out What Insurance Coverage You Need

Here are a few steps you can take today to assess your insurance needs:

Most full-time employees will receive at least some forms of insurance from their employer. Make sure that you understand what coverage you do and do not have, and the level of protection that you have. Reach out to your HR department if you aren’t able to locate the relevant information yourself

If you’re not covered for certain types of insurance, or don’t have a satisfactory level of coverage, consider reaching out to an insurance broker to discuss your options

It’s far too easy to push the topic of insurance down to the very bottom of your priorities list, but keep in mind — the time to repair a roof is when the sun is shining.

Moonshine Money: A Do-It-Yourself Guide to Personal Finance

Once you get a hang of the core personal finance skills (budgeting, reducing debt, investing), your net worth will start to tick up higher and higher with each passing month. Learning to identify financial fraud, tricks, and scams is an important part of protecting the nest egg that you’ve built up.

According to CNBC, 15.4 million consumers in the U.S. were victims of financial fraud in 2016. In total, these victims lost $16 billion.

With great wealth comes great responsibility.

Be Prepared

Scammers are constantly dreaming up new ways to defraud unsuspecting victims, but there are several common threads that you should be aware of:

Commons Scams and Frauds from USA.gov: a good run-down of many typical tricks that scammers try to play

The more you understand the fraudster’s standard playbook, the better prepared you’ll be to avoid falling into their trap.

Stay Skeptical

Whenever you’re presented with a financial opportunity such as an investment in a new business or a unique way for you to invest your money, ask yourself: How will the other party in this transaction make money?

People who give things away for free tend to not stay in business very long. If it’s not clear how they make money, they’re probably making money off of you.

A healthy dose of skepticism goes a long way.

If you get a suspicious phone call, letter, or email, keep these tips in mind:

10 Tips To Avoid Common Financial Scams – a good list of best practices to follow to reduce the risk of being de-frauded and/or having your personal information stolen

How to Secure Your Accounts with Better Two-Factor Authentication: As our digital and financial lives increasingly go digital, securing access to your online accounts is critical. Two-factor authentication is a recognized best practice for adding an extra layer of security

Scammers will often try to drum up a false sense of urgency in order to trick you into making a snap decision. Don’t fall for this.

If you find yourself in an unusual situation involving money, ask for a few minutes to think through the situation. Ask questions, and don’t be shy to tell them to call back later.

Stay safe!

Moonshine Money: A Do-It-Yourself Guide to Personal Finance

This course stands on the shoulders of giants. The online resources listed below have been instrumental in my own journey to learn about money management. Each of these resources is a seemingly never-ending source of informational golden nuggets.

You can learn whatever you wish if you’re willing to read, read some more, and absorb. This is as good a place as any to start…

General Personal Finance

Reddit Personal Finance community: A great forum to discuss the broad topic of personal finance, from budgeting to home buying, insurance, investing, retirement, taxes, and more. Get quick answers to nearly any personal finance topic. Note that this forum is quite US-centric

Bogleheads forum: An incredibly deep body of knowledge on investing. A fantastic place to learn a thing or two (or 100) about building wealth. Written by disciples of John Bogle – founder of Vanguard and inventor of the first index fund

Canadian Couch Potato: The best website to learn about passive investing in Canada. Great tips on asset allocation, fee reduction, and general investment tips. Check out their “Model Portfolios” page for a simple guide to building your investment portfolio.

Frugality

Budget Bytes: Delicious recipes at low cost. Each recipe includes a total cost / cost per serving estimate. My personal favourite is the rosemary garlic beef stew recipe @ $1.41 per serving

Reddit Meal Prep Sunday community: An overflowing supply of meal recipes that are easy to cook in large batches (and tasty!). A great intro to the world of “meal prepping”

Financial Independence / Early Retirement

Mr. Money Mustache: Musings from a guy who retired at the ripe age of 30. No shortage of tips on how to reduce your spending drastically. MMM was not the original early retiree, but has arguably done more than anyone to bring the concept of early retirement into the mainstream

Frugalwoods: A look into the life of a family that simplified their life in the big city to live on a homestead in rural Vermont

Reddit Financial Independence community: Thoughtful discussion on quantitative early retirement strategies, preparing for the mental & behavioural side of early retirement, and life after retirement. Over 400,000 readers and contributors

Early Retirement Now’s ultimate guide to safe withdrawal rates: If you’re interested in early retirement, you’ll soon come upon the concept of a “safe withdrawal rate”. For the definitive guide on SWRs which will answer all the questions you currently have and ever will have, look no further

Moonshine Money: A Do-It-Yourself Guide to Personal Finance

What follows is a list of books which heavily shaped my views on personal finance. While I’ve tried to distill the ideas from these books into this course, reading these classics first hand would be an investment that pays off time and time again.

In the spirit of good money management, I’d encourage you to borrow these books from your local library. If you’d like to purchase a copy instead, I’ve included links from Indigo (for Canadians) and Amazon where you can do so.

Your Money or Your Life – Vicki Robin and Joe Dominguez

Vicki Robin and Joe Dominguez were the originators of the Financial Independence movement.

This groundbreaking book is guaranteed to change your stance on all things money. It’s a marvelous testament to frugality and aligning your spending to your life’s values.

If you want to spend less money, spend more time with friends & family, diminish your reliance on your day job, and get off the treadmill that always leaves us wanting more — this is the book for you.

There’s more to life than “nine to five till you’re sixty-five”.

The Little Book of Common Sense Investing – John Bogle

A guide to everything you need to know about investing. A short, sweet, and impactful read.

The book’s author John Bogle – the founder of Vanguard and creator of the first index fund – is considered to be one of the most important contributors to modern finance. In 2017, Warren Buffett wrote:

If a statue is ever erected to honor the person who has done the most for American investors, the hands-down choice should be John Bogle. For decades, John has urged investors to invest in ultra-low-cost index funds. In his early years, John was frequently mocked by the investment-management industry. Today, however, he has the satisfaction of knowing that he helped millions of investors realize far better returns on their savings than they otherwise would have earned. He is a hero to them and to me.

If you’re currently invested in actively-managed mutual funds, or are considering doing so, please read this book. The case for investing in low-cost index funds cannot be made better.

The Millionaire Next Door – Thomas Stanley & William Danko

The authors of this book interviewed and studied over 1,000 millionaires in order to find out what it takes to become wealthy. The big takeaway? The popular perception of millionaires doesn’t match the actual behaviours of typical millionaires.

This book shatters the urban myth that millionaires live flashy lifestyles (high fashion, luxury cars, mansions, etc.). In fact, the typical millionaire is more likely to resemble your next door neighbour.

Wealth isn’t driven by how much money you make or how much you spend. Wealth comes from the amount of money that you accumulate (i.e., save).

This book will give you a “light bulb” moment on the mindset side of building wealth. You don’t need to spend money to make money. You don’t need to flaunt your money by buying high-priced status symbols. The more you earn, the more you should save each year.

Starting a family — it’s a roller coaster of new experiences, proud moments, and obstacles to overcome. So much will change; your priorities, sleep schedule (oh how it will change), and daily thoughts.

And, it just might be the most rewarding challenge that you ever undertake.

Before you start on the journey, it’s important that you also take time to consider the financial angle of starting a family.

The Cost of Raising Children

I’ll dispense with the scary bits first: raising children is an expensive proposition. The U.S. Department of Agriculture estimates that a middle-income family will spend an average of $12,980 per year to raise one child, not including any savings for college. Up to the child’s 18th birthday, this is a total cost of $233,610 (per kid).

Let’s pause here so you can take a few deep breaths.

To be honest, big bold headline numbers like that aren’t particularly helpful. The cost of raising children will be different for each and every family.

For example, if the home you live in has enough space to accommodate your expanding family, your costs would decrease considerably. Note that 29% of the total cost estimate from the USDA comes from additional housing costs.

For a glimpse into the day-to-day life of families raising children, check out:

Apathy Ends’ round up of the first year of raising their child. I hope you like Moana…

She Picks Up Pennies’ calculation of the weekly cost of raising her three-month old child

Each and every family’s situation will be unique, but you owe it to yourself (and your little one) to get prepared for the exciting changes to come. Good luck 🙂

Moonshine Money: A Do-It-Yourself Guide to Personal Finance

For many people, homeownership ranks near the top of their financial goals. Buying a home is seen as a major milestone in life. You get a job, buy a home, start a family, then your kids go out and do it all over again.

Unfortunately, in many cities around the world the prices of homes have been rising at an unsustainable rate, far outpacing increases in income. Buying a home has become an incredibly expensive proposition. It’s a financial decision that should be considered carefully.

For those who plan on buying a home in the near future, I’d suggest the following:

Run the math on renting vs buying — you may be surprised by the result

If you’re still in favour of buying, make sure you understand the “all-in” costs of homeownership

Create a savings plan to get you there

The Rent Versus Buy Debate

The debate over renting or buying a home is a classic argument in the personal finance world.

Common wisdom holds that “buying is always better than renting”, or “renting is just flushing money down the drain”. It’s simply not that simple.

The truth is that in some scenarios, buying a home is better than renting, and in someother scenarios, renting a home is better than buying. I know it’s not a satisfying answer, but it’s the reality. Depending on the assumptions (home purchase price, home price appreciation rate, mortgage interest rate, rent price, opportunity cost of your down payment), the answer can swing either way.

As a result, it’s very important that you run the math on whether buying is a home is better than renting a comparable home. You can use this calculator which I’ve built to run that Rent vs Buy math. You should try out a few different scenarios so that you get a good sense of how much the answer can change even after making small tweaks to the assumptions.

Once you realize that either renting or buying can be the better long-term financial decision, it becomes clear that this decision is mostly a lifestyle choice. I’ve written further on this in my article, The Soft Side of the Rent versus Buy Equation.

The point being — give the option of renting a fair shake. Don’t blindly assume that buying a home is always a better financial decision.

The “All-In” Costs of Homeownership

While the cost of a mortgage may be the biggest cost when buying a home, it’s far from the only cost that you’ll incur. Before making the decision to buy, be prepared for the other “hidden” costs of homeownership:

Property taxes

Maintenance and repairs

Homeownership’s insurance

Condo fees / Strata fees / HOA

Closing costs to buy a home (legal fees, home inspection, land transfer tax, etc.)

Costs to sell a home, if and when you move (broker’s fee) — often ranges from 4 to 6% of the total home sale price

Over and above your mortgage, this can add up to thousands of dollars when you first buy your home, thousands of dollars per year in ongoing costs while you own your home, and tens of thousands of dollars when you eventually sell your home. These costs are definitely not a rounding error that you can sweep under the rug.

Make sure that you do your research so that you can reasonably estimate what these costs might be. It would be worthwhile to talk to other homeowners in your area to get a sense of what these costs might be.

Now that understand what the “real” costs of buying a home are, its time to put a savings plan in action.

I firmly believe that you should target to save up a down payment of at least 20% of the purchase price. By doing so, you’ll avoid paying for mortgage insurance (called “CMHC” in Canada; “PMI” in the U.S.). If you don’t have a 20% down payment, you’ll need to delay your purchase so that you can continue saving up, or adjust your expectations downwards and opt for a cheaper home.

In addition to the down payment amount, you’ll need to save a few thousand dollars extra for your closing costs (legal fees, home inspection, land transfer tax, etc.). Before jumping in and making an offer on a home, talk to a local real estate lawyer to get a sense of the typical range of closing costs in your area.

To summarize: your target savings goal should be 20% of the purchase price of the home plus a few thousand dollars for closing costs. To meet your savings goal, consider setting up regular automatic deposits and bear down until you get there.

While you’re saving up for your home downpayment and closing costs, this money should be held in low-risk investments such as a high-interest savings account. Your home purchase fund should not be invested in the stock market.

As discussed previously in this course, stocks can be extremely volatile in the short term. If you invest your house fund into the market, you risk losing 40%+ of your money when it comes time for you to buy a home. Not a great idea. Since you need this money in the short term (<5 years), the prudent move is to forfeit the potential investment gains, and keep your money invested in something offering low risk and low reward.

Moonshine Money: A Do-It-Yourself Guide to Personal Finance

Build the life you want, then save for it. It’s a simple phrase that I loved from the moment I read it, and it’s something I find myself re-visiting often.

Now that you’ve come so far, I think it’s important to take a step back and critically evaluate your relationship with money. Having gone down the path of learning about, controlling, and ultimately amassing money, you might find that saving more and more money becomes a goal onto itself — an obsession even.

It seems ludicrous to caution someone against saving too much money, but it can and does happen (the post linked above is just one of many examples).

When you seek money as an end goal rather than a tool to achieve something else, it can lead to unhealthy habits. Checking investment account balances daily; declining invitations from friends and family to avoid spending on food & drink; cutting out hobbies that you deem “too expensive”; making yourself unhappy to pad your bank balance.

To guard against this, I recommend adopting a “conscious living” mindset. At its core, this means living a life where all of your choices have been made deliberately.

Build The Life You Want

Try to imagine what a happy and satisfied life would look like for you, taking money entirely out of the equation.

Where do you live? What type of food do you eat? What clothes do you wear? What hobbies and passions do you have? How often do you travel and to where? In essence — if you didn’t have to work for money, what would you do with your time?

Some people might want to spend their days jetting from one continent to the next, others may want to stay at home reading and playing video games. Neither of those lifestyles is more virtuous or “better” than the other. They are both valid choices,

Keep an open and conscious mind and decide for yourself. If it’s what you want, it’s what you want. What anybody else thinks doesn’t matter one bit.

As much as possible, try to start building that life now. Take small steps towards the goal, starting today. Devote an hour or two each week to trying out a hobby you think you might be interested in. Plan a weekend hiking trip at your local mountain.

Perhaps you’ll find a passion that brings you real joy. And what if it’s expensive? So be it. Weigh the benefits to your happiness against the financial costs, then make a deliberate choice.

Spending money on things or experiences that make you happy is absolutely OK. Frugality is not an inherent virtue.

Don’t wait for a distant future to start building the life that you want. If you wait too long, you might find yourself rich, lonely, and bored.

Start to sketch it out now — you can fill in the details later.

Save For It

Before you buy a boat and sail off into the sunset, keep in mind the second half of the mantra — build the life you want, then save for it.

In the spirit of conscious living, we also need to be mindful of the financial impact of the decisions we make. The life that you’ve chosen for yourself has a price tag attached to it.

Saving up for the life you want might require a higher income, a delayed retirement, or cutting back on other expenses that don’t fit into your long-term plan.

Don’t kid yourself, if luxury vacations are a part of the life you want, you need to include that in your budget and save for it.

Once again, spending $20,000 a year isn’t necessarily “better” than spending $100,000 a year (or vice versa). The more expensive your lifestyle, the more money you’ll need to save up to sustain that lifestyle. And that’s fine.

Everyone is different — find out where you’d like to position yourself on the spectrum, and plan accordingly.

Say it with me one last time: build the life you want, then save for it.

Moonshine Money: A Do-It-Yourself Guide to Personal Finance

Numbers are only half the battle. In some senses, getting a grip on the numbers side of personal finance is the easy part. Once you learn the mechanics, you’ll need to work to develop apositive money mindset. This will help you to stay motivated through the journey and allow you to have a healthy relationship with your money.

As your financial literacy increases, you might get drawn into the rabbit hole of learning about minor financial optimizations or trying to squeeze every last drop out of your dollars.

If that’s what you want, all the power to you. However, for others, this can lead to stress, obsession, and burn out.

Below, I’ve listed a few core principles that have helped me to build a positive money mindset. I hope that they’ll be of good service to you as well.

Don’t Let the Perfect Be the Enemy of the Good

Or put differently:

“Better a diamond with a flaw than a pebble without.”

The sooner you realize that your financial plan doesn’t need to be perfect, the better. Follow the 80-20 rule: chase after the big wins first, and don’t get hung up on the little things that remain.

Focus on:

Tracking your spending regularly (cash inflows and outflows)

Paying off debt

Spending less than you earn

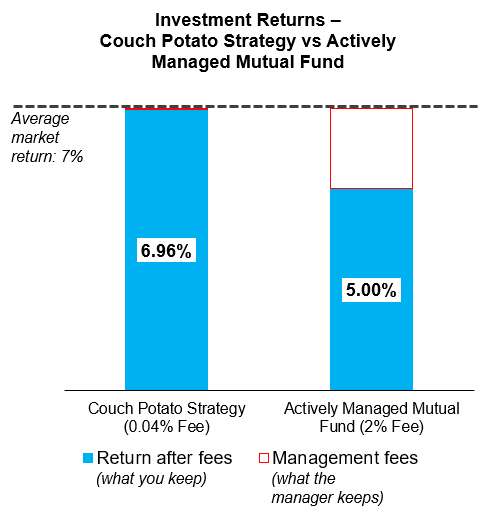

Investing the difference wisely (using a couch potato strategy)

Once you’ve mastered these core skills, the rest is small potatoes. Perhaps you should be investing in your RRSP instead of your TFSA (Traditional vs Roth for Americans), perhaps your allocation to international stocks should be slightly higher than it is today, maybe!

These are complicated topics that you don’t need to understand fully at this point. You can figure that out later. Master the core pillars first, and then worry about everything else later (or never).

Keep It Simple

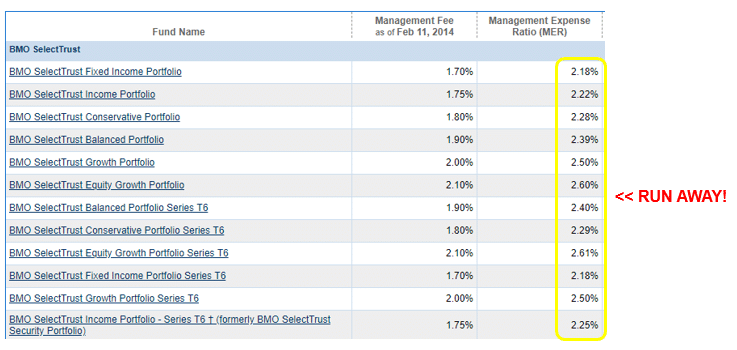

You don’t need to own 12 different investments funds so that you can get exposed to every niche investment asset class (gold, real estate, German tech stocks).

Don’t over-complicate your financial process. Set a regular schedule of sitting down for a couple hours every month to tackle all of your financial to-do’s. Obsessing over the tiny details might bring about a small improvement, but it has a greater chance of making you burn out and lose your positive momentum.

Get a hang of the basics of budgeting. Make some efforts to cut back on the major expense items of housing, transportation, and food. After this, diminishing returns start to kick in — don’t fret about the coffee you bought yesterday or the $5 discount that you missed on your gym membership.

Make Gradual Improvements

Rome wasn’t built in a day. Likewise, it’ll take quite a bit of time for you to go from being underneath credit card debt to having maxed-out retirement accounts.

Trying to make too many changes all at once will leave you stressed and unmotivated.

Take your time — learning the mechanics of money management and changing your attitude towards money can take months or even years.

Sketch out a rough plan with your target milestones, and take it one step at a time. This isn’t a race, go at your own pace.

Break down your plan into bite-sized chunks (understanding your paycheck, opening a savings account, tracking your spending for one month, opening an investment brokerage account, making your first trade, etc.).

As you start to rack up small wins, you’ll find the motivation to keep checking items off of your list.

Comparison Is The Thief of Joy

No matter where you are on the spectrum of financial literacy, you’ll always be able to find someone who has accomplished more.

I promise you that there’s someone out who’s younger than you, earns more than you, spends less than you, and still manages to jet off on instagram perfect vacations — all at the same time.

Comparing yourself to these people is simply unproductive. You’ll only be hindered by starting to question your decisions and your progress to date.

Everyone was born with different advantages, had a different upbringing, and has benefited from lady luck in a different way. “Some people are born on third base and go through life thinking they hit a triple”. It’s impossible to adjust for all of these factors to make an apples-to-apples comparison.

Comparison is the thief of joy. At worst, it can lead to a vicious cycle of low self-esteem and a desire to stop thinking about money at all.

Focus on your own journey. Take it slow. Focus on putting one foot ahead of the other, over and over again, and I promise that you’ll reach the summit.

Conclusion

Yes, the dollars and cents aspect of personal finance is important. You won’t be able to meet your goals without a solid grasp on budgeting and investing. But the mental aspect is just as important.

Spend the time and effort needed to develop a positive money mindset. You’ll feel happier about your money, and will retain the spark you need to follow your plan through to the end.

Moonshine Money: A Do-It-Yourself Guide to Personal Finance

Increasing your income can have a huge impact on the time it takes to reach your financial goals.

Most people will find it incredibly difficult to cut out $5k or $10k of annual expenses from their budget (there are only so many lattes that you can stop drinking).

However, some people will be able to negotiate a raise or find a new job that would bump up up their income by many thousands or even tens of thousands of dollars.

To be clear, this is not for everyone. There are many industries or careers where your salary is based on a pre-determined grid. Jumping to a new employer or negotiating harder won’t yield any results in some cases. If it’s not possible to increase your income, you’ll still get to where you want to go by focusing on the core personal finance skills — budgeting, spending less than you earn, and investing wisely.

With that said, let’s discuss the steps you can take to jump on the rocket ship to financial freedom by increasing your income.

Know Your Market Value

We need to walk before we run. Before you can make any radical changes to increase your income, you’ll need to understand how your current income compares against people working in similar companies / departments / jobs.

To get a sense of the market salary range for your job, try out these resources:

AngelList (for startup jobs specifically — all job offers have salary ranges listed)

For Americans: Check out this fantastic interactive map from the Hamilton Project, which allows you to see salary data with filters for job titles, age, and location. A pretty amazing data set.

Try searching for a few variations of your job title (companies tend to use slightly different terminology to describe the same job). Your goal should be to find out what the typical salary range is for your type of job (low, average, high).

Where do you fit in the salary range?

Figure Out What You Want

Spend some time to figure out what you want next in your career. Are you happy with your current path, but want to move up the ladder? Do you want to jump ship to do the same job at a better company? Do you want to try out something entirely new?

What would your dream role would look like? What are the key areas where your current job is lacking in (pay, type of work, seniority, work-life balance, team, purpose, autonomy, etc.)? Which companies would offer a better overall role?

Try to sketch out an outline of what you want.

Use those same salary research tools above to get a grasp on what the pay range is for a few of the jobs you’d be interested in.

Don’t skimp out on the effort here. The decision of where you’ll work for 40+ hours a week, week after week for years (or decades), is not one to be taken lightly.

Informational Interviews 101

To get in in deeper than what’s available on the internet, and to increase your job switching prospects, I highly recommend setting up a few informational interviews.

An informational interview is a quick chat with somebody (over the phone, in person over a coffee) where you’re trying to learn about their industry, what their day-to-day job is like, good ways to break into their company, etc.

The goal of an informational interview is well, information. You’re not trying to immediately leverage this into a job offer. Instead, this is a great opportunity to expand your network, learn about a new industry, and ask some basic questions.

A quick primer:

Start with your existing network of friends, family, and acquaintances — can you easily reach out to anyone that works in an industry you’re interested in?

If no luck there, try to find someone on LinkedIn. Use the search function to look for people working at relevant companies, and try to find someone that you have some mutual connection to (went to the same school as you, friends with someone you know, etc.)

Any way you can, gather up a list of a few people you’d want to meet with, and send off a message to them. For best results, try to get introduced by a mutual contact. Otherwise, an email or LinkedIn message out of the blue works as well

Mention that you’ve been doing some research into their industry or company, and have been considering a potential move in the future. Ask if they’d have 30 minutes in the next week or two to chat with you about some questions you had about their company and the industry as a whole. Be polite and flexible!

For the informational interview itself, make sure you do your research beforehand on this person’s background, what their company does, and come ready with some general questions about the industry. Try to find a few news articles about emerging trends or developments in their industry — you can base your questions on what you learn here. The idea is to show that you’ve done your homework and have a genuine interest in what they do

Try to find out how this person got a job at the company they work at. Do they have tips for someone trying to break in? What are the hard and soft skills necessary to succeed?

At the end of the interview, ask them if they could recommend a couple of people that you could reach out to in order to continue learning about the industry. Would they mind introducing you over email?

If all goes well, you’ll be able to schedule more informational interviews. Keep the ball rolling until you know enough to make an educated decision about whether you’d like to pursue an opportunity in this industry in the future

Depending on how the conversation is going, it may be appropriate for you to mention that you’re really interested in the industry, and would love to hear if their company or other similar companies have any roles open

Always keep in mind that the person chatting with you is doing you a big favour by taking time out of their schedule to meet. Offer to buy their coffee; don’t be too pushy asking about job offers; send a “thank you” note to follow up

By the end of this informational interview process, you’ll have met plenty of people actually doing the job you want, and you’ll be ready for interviews. You will be miles ahead of the competition if you decide to switch.

Keep Your Options Open

Be open to new opportunities even if you’re happy today with your company / salary.

The best time to look for a new job is when you already have one. This allows you to be patient and picky with new opportunities, instead of being forced into accepting the first offer that pops up.

Keep in mind that your work situation can change on a moment’s notice. The boss that you get along with could get replaced by someone who drives you insane. Your company could get acquired, making your job redundant. Colleagues change, company budgets change, you just never know.

You can even go as far as interviewing for jobs that you don’t really intend on taking. You’ll keep your interviewing skills sharp, get to know your market value, and will have the opportunity to make a change when it suits you.

Negotiate Raises At Your Current Job

Negotiating salary at your current job is tough, but is definitely well worth it. A 15-minute conversation could be worth thousands of dollars a year.

Some tips for getting a raise during your next annual review:

A couple of months before your annual review, give your manager a heads up that you want to discuss compensation at your review. By planting the seed now, your manager will be prepared for the conversation and may discuss this in advance with the HR department to secure a raise for you. If you just spring it on your manager at review time, their budget may already be locked down, meaning you’ll have to wait until next year

When it comes time to speak with your manager, go in prepared with a list of factual reasons why you should be getting paid more. Some example: market benchmarks for compensation, how your job responsibilities compare against the average worker in this role, why your performance merits an above market salary. It needs to be clear and logical why you deserve a higher salary — don’t just ask for more money just because

Be polite and non-confrontational. Don’t turn this into a personal fight

Try framing the discussion as: “what do I need to do to get the raise I’m asking for?” This way, you and your manager can be on the same side in figuring out what would need to change for you to receive the pay you want

Know your next best alternative — will you accept a hard no? Do you have a minimum raise you want? Will you move to a new role if they say no?

As always, know your market value before you walk into any negotiation.

Negotiating Salary At a New Job

If you’re moving to a new job, this the absolute best time to negotiate. They have a role that they’re trying to fill, providing you with quite a bit of leverage.

Pay is undoubtedly important, but be creative. You can also score wins on vacation time, work from home privileges, remote work, expense reimbursements (moving expenses, cell phone, car).

For some great tips on negotiating when you move to a new job, read through:

Getting an advanced degree in your current field, or studying something entirely new can be a great way to increase your income. Taking time to go back to school can be incredibly rewarding on an intellectual level, and a healthy reward for your paycheck as well. People with grad degrees are typically paid more and are likelier candidates for promotions.

But, just hang on for a little before you trade in your briefcase for a backpack. Going back to school can be incredibly expensive. Starting with tuition, and lumping on foregone income and student loan interest turns this into a sizeable check.

Use glassdoor / payscale to research your current role (use different word combos since the same job can be called different things) and find out what the market rate for your job is (low, average, high)

Keep your resume up to date; after finishing a big project, work that into your resume; this way, your resume will be fresh and ready to go if an opportunity pops up

Spend some time brainstorming about new jobs that you’d be interested in (either similar to today or completely different)

Set up some information interviews with people working at companies / in industries that you want to pursue

Negotiate your salary (whether at your current job, or especially if you move to a new job)

Moonshine Money: A Do-It-Yourself Guide to Personal Finance

If you want to accelerate your progress towards your financial goals, reducing your expenses is the best place to start. The amount that you spend is fully within your control. Implement a change in your lifestyle and you’ll see the results immediately.

I think it’s well worth it for everyone to make an honest assessment of their spending habits. I’d wager that most people are spending money on things that don’t improve their quality of life.

Cutting back on your expenses (even just for a few months) can bring about some major benefits:

You’ll be able to find out what things and experiences are truly important to you. You might find that you don’t even notice it when you cut something out of your life

When you find out what things really are important to you, you’ll have a greater appreciation for those things when you start to spend on them again. It’s awfully easy to settle into a rhythm and start to take things for granted

By making a shift to live more frugally for a period of time, you’ll reset your habits and defaults. This can have a long term impact on your spending habits

Down below, we’ll look at the major expense categories for most people (home, transportation, food) and discuss how you can reduce those expenses.

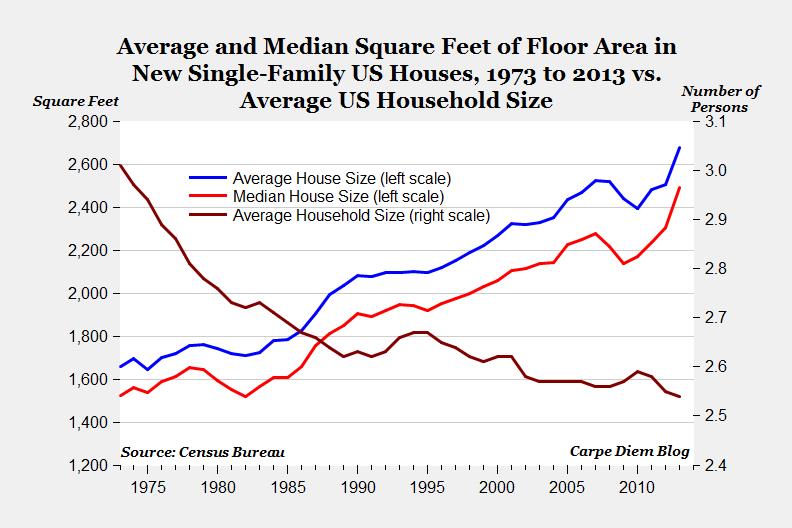

Downsize Your Home

Ask yourself: does the home that I live in right now really need to be this big?

Society’s perception of a “normal” house size has shifted considerably in the past few decades. From 1973 to 2013, the average size of a new single-family house in the US has increased from ~1,600 square feet to ~2,600 square feet.

This huge increase has come at the same time as the average number of people in each household has decreased from ~3 to ~2.5 per home.

If you choose to live in a large home, just remember that you’ve made a deliberate choice to live in such a way, and that your choice has a price tag on it.

Lose the Car

Cut back to one car, or no cars if possible. If you can manage it, biking to work is great way to reduce expenses, stay fit, and protect the environment — all in one stroke.

Taking public transit is another great option. Bring your favourite music and/or podcast along for the ride, and forget the stress of having to navigate through rush hour traffic.

Use a trial period to see if you’re willing to make this lifestyle change. Switch out your car commute for a bike / public transit commute for a few weeks, and see how you feel.

At worst, you’ll save on gas costs for a bit, and you’ll have given the alternatives a fair shake.

Meal prepping

Meal prepping (making a large batch of food in one sitting) is a great way to reduce your spending on eating out at restaurants.

It took some time getting used to it, but it’s now part of my regular routine to make 6-10 meal portions on Sunday night. It’s become extremely rare for me to buy lunch at work. A couple of great resources for meal prepping:

Budget Bytes: Delicious recipes at low cost. Each recipe includes cost per serving estimate. My personal favourite is the rosemary garlic beef stew recipe @ $1.41 per serving

Reddit Meal Prep Sunday community: A seemingly limitless supply of meal recipes that are easy to cook in large batches (and tasty!). A great intro to the world of “meal prepping”

Before You Make a Big Purchase

Before you make a big purchase (new TV, car, couch, clothing, etc.), force yourself to wait for 2 or 3 days before you go ahead and actually buy it. You might be really excited in the moment at the store, but find that you don’t actually want that thing once you’ve had the chance to sleep on it.

This will help to limit impulse purchases that you’ll regret down the road. Take some time to think about if that thing will make you happy, if a cheaper option would also tick the boxes you’re looking for, and if you think you’ll get good use of that thing.

Then ask yourself: do I actually want to buy this, or am I tempted to do so because everyone else is doing it (friends, colleagues, family, etc.)?

Remember that most people are terrible with their money. The average person lives paycheck to paycheck, doesn’t have an emergency fund, is entirely reliant on their job, and doesn’t have any real plan to meet their future financial goals. Don’t spend like everyone else.

Finally, is there any way of buying this second hand? If you do some searching around online (Craigslist, Kijiji, Facebook Marketplace) and in your local thrift store you can often find some great secondhand deals on:

Home goods (tables, chairs, lamps, dressers)

Clothing (lots of like-new clothing, high quality vintage items, or expensive brands at cheap prices)

Stereos and sound systems

Used bikes (lightly used at less than 50% of the price of a new bike)

Books and records

Lots and lots more

Hobbies, Activities, & Entertainment

Finding a hobby that you look forward to doing everyday is something I’d encourage everyone to do. Carve out some time during the week or weekend to try new things, pick up new skills, or learn about something that interests you. You just might find a passion that you can carry forward for the rest of your life.

What follows is an entirely non-exhaustive list of activities that are fun and frugal…

It is free to:

Take out books, music, and even DVDs from the local library. Free access to limitless sources of knowledge, and/or just a great way to pass the time. It is well worth it to be acquainted with your local library branch

Visit a nearby park. Stroll around, take a few deep breaths of fresh air, and soak up the sounds of nature

Attend events hosted by your city. Most cities put on free activities such as festivals, concerts, walking tours, yoga in the park, etc.

With low start-up and ongoing costs, you can:

Learn piano, guitar, or your instrument of choice. It’s hard to match the rewarding feeling of improving each and every day on your own accord. Lots of fun to be had in performing for others as well

Purchase a used bike, and embark on adventures exploring your own city and thereabouts

Pick up a chess board and a few beginner’s books. Chess is a personal favourite hobby of mine. You can spend decades learning and honing your skills, and still get beat by a 12 year old Russian kid 🙂

Learn to cook tasty, healthy, and affordable meals. It may seem daunting at first, but cooking can become a really fun activity that is rewarding and frugal. Hosting your friends for meals & potlucks is another upside

You’ve flipped the switch on your financial auto-pilot; you see a steady stream of money building up each month; you’re probably itching for the next step. Now what? In this lesson, we’ll discuss setting financial goals.

Having clear goals in mind will keep you accountable to your plan and will help you to figure out how much (and why) you need to save.

What Are You Saving For?

By setting financial goals, you can turn your savings & investment account balances away from just being abstract numbers on a screen into something much more tangible. Each of your dollars will have a purpose:

Paying down student loans / credit card debt

Savings for the big trip you’ve always wanted to take

Home down payment fund

College savings for your children’s education

Retirement nest egg

Spend some thinking about what your personal financial goals are. Think immediate (this month), short term (1-12 months), medium term (1-5 years), and long term (5+ years).

Totally fine if your goals are vague rough outlines at this stage. The point is to give yourself something to work towards.

There are worse things in life than saving up a few thousand bucks for one purpose and then changing your mind once you get there.

What If I Don’t Know What My Goals Are?

What if you still find it difficult to sketch out long term plans and goals? Perhaps you’re comfortable with your life now, but have too many uncertainties on the horizon — will I move to a new city? Do I want to have kids down the road? Will I eventually buy a home?

If the view is too hazy to lock down on concrete goals at the moment, I’d suggest setting your sights on attaining “financial independence” — also known as “F-you” money.

A financially independent person is someone who can choose to:

Refuse to tip-toe around others at work — you can speak up when you feel strongly about something, say “no” to your boss, generally walk a little taller in your shoes

Ask for reduced working hours or a fully remote job (if that floats your boat)

Work at a job that aligns strongly with your values, even if this means taking a big pay cut

Take time off work to re-charge; travel; pursue a passion; make music; play video games; whatever!

To put it more bluntly: once you’ve got enough money you can say “F-you” when, where, and to whom you want. Having more money makes you less dependent on others. More money = more freedom.

The bottom line: Spend some time thinking about why you are saving your money. Set your sights on the goal and make it happen.

Moonshine Money: A Do-It-Yourself Guide to Personal Finance

I don’t know about you, but I can think of at least a few things I’d like to do rather than checking bank account balances, budgeting, and making trades in my brokerage account.

Fortunately, it’s possible to automate some aspects of the financial process. Think about this as flipping the “auto-pilot” switch on, so that you can spend less time and mental energy thinking about your money.

For me, I’ve settled into a rhythm of checking my account balances every couple of weeks (more out of curiosity than anything), and spending about a couple hours every 2-3 months to update my budgeting spreadsheet and make trades in my investment account.

I don’t feel stressed or burdened at all by this process. If you follow the steps below, I’m confident that it’ll be the same for you as well.

Pay Yourself First

“Paying yourself first” is an extremely simple and effective strategy that can help you meet your savings goals. The idea is that you spend what is left after saving, and not the other way around.

For example, let’s say your bi-weekly paycheck comes out to $1,500, and your goal is to save $300 out of each and every paycheck.

If you follow the pay yourself first methodology, you’d set up an auto-deposit for $300 on the day that your pay check comes in. This money could be directed to your emergency fund account, to your student loans, or to your investment brokerage account (whatever your goal is). In any case, this money is out of sight, out of mind.

With the $1,200 of your paycheck that remains after the auto-deposit, you’re free to spend that money however you choose. You don’t need to feel guilty if you order take-out or buy a new pair of shoes — as long as you manage to stay within your $1,200 budget, you’re good to go.

Save first, and spend what is left after saving.

The real power of this simple strategy is that you’ve managed to meet your savings goal without having to lift a finger or make any decisions. By automating your financial processes as much as possible, you give yourself the best chance of sticking with your plan in the long-run.

The alternative is to save what is left after spending. In that case, you’ll need to constantly monitor your purchases to make sure you’re not going off track. A night out with friends here and an impulse purchase there, and you might find that you’re short of your savings goal at the end of the month. Not fun, and not a recipe for success.

Pay yourself first, and you’ll make your life much easier.

Pre-Authorized Payments

Most companies that send you a bill on a regular basis will offer a “pre-authorized payment” option. By signing up for this, your bill will be paid automatically, without the need for you to manually log in and send your payment.

By doing this, you can stop worrying about missing a payment and being charged late penalties.

Personally, I’ve set up pre-authorized payments for my:

Monthly subway pass

Hydro bill

Internet bill

Credit card bill

If you go down this route, make sure that you regularly review your credit and debit card statements. Watch out for any unusual charges on your statement.

Your Assignment

For your main bank account where you receive your paychecks, find out what “auto-deposit”, “auto-transfer”, or “automatic savings” options are available. Typically, you’re able to set up a recurring auto-deposit schedule specifying where the money should be moved to, the $ amount to be moved, and the frequency (every week / two weeks / month, etc.)

Decide on the amount of money you can comfortably set aside from each paycheck. Set your auto-deposit amount at a level that will leave you with enough remaining to cover your necessities and a reasonable amount of “fun spending”. You may consider starting your auto-deposit amount relatively low until you get a hang of it, and then ratcheting it up as time goes on

Pro tip: if you get a raise at work, immediately increase your auto-deposit amount. This way, you can increase your savings without ever being tempted to spend away your larger paycheck

For American readers: brokerages such as Vanguard offer the option of “automatic investing”. This is an amazing feature and takes automation one step further. After your money is automatically deposited into your Vanguard account, you can set up rules so that this new money is invested according to your chosen asset allocation. This means that you don’t have to manually make your trades. I’d highly recommend setting this up so that you can maximize your “time in the market”. Making your life much easier is another nice upside.

For Canadians: unfortunately, our financial scene is lagging behind the States and there aren’t any options to do automatic investing in a portfolio of index funds. I’m waiting patiently…

Moonshine Money: A Do-It-Yourself Guide to Personal Finance

Now that you’ve settled on the index funds (a.k.a. ETFs) that you’d like to invest in, we’ll go through a step-by-step tutorial on the mechanics of how to trade online, so that you can start putting your money to work.

To illustrate, I’ll be making a trade in my Questrade brokerage account, so you’ll see some visuals from that trading platform. If you’re using a different investment broker, it will look slightly different, but the broad concepts are the same.

Side note: If you’d like to open a Questrade DIY (Do it Yourself) account for low-cost index investing, please feel free to add my referral code of 336413903418268 when you open the account. We will both receive $50 in that case!

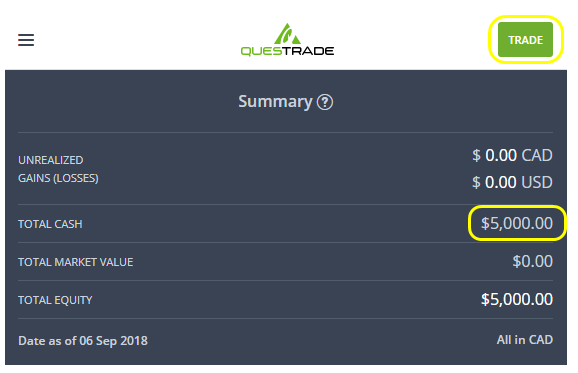

After logging into my brokerage account, first I see a summary of my portfolio. I’ve got $5,000 of cash in the account, and would like to use that money to purchase some investments. Click the “Trade” button at the top right to start.

Step 1 – Look Up the Correct Investment Symbol

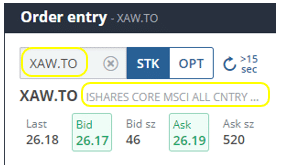

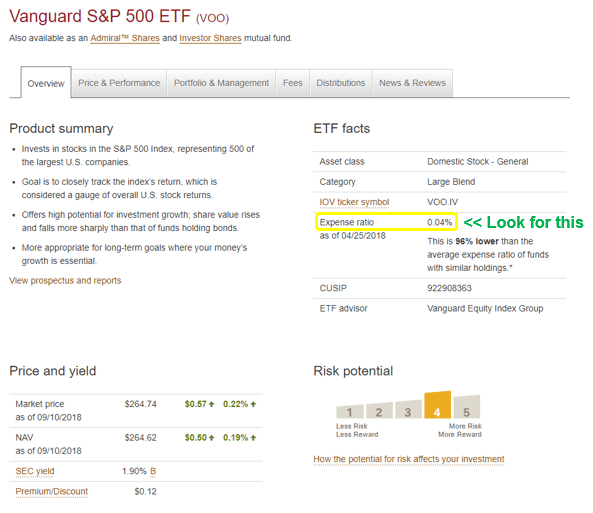

Index funds are typically identified by a three to five capital letters (VCN, XAW, VAB, VOO, VTSAX, etc.). Based on your chosen asset allocation, you need to identify which index fund you want to purchase. Based on my investment plan, I’d like to use my $5,000 to buy shares in the index fund XAW, a fund holding shares of companies from all around the world, but excluding Canada.

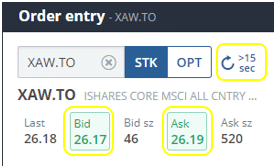

In the order entry section on the right side of the page, I type in “XAW”. Questrade actually identifies this fund as XAW.TO since it trades on the Toronto Stock Exchange. Beside the investment symbol (also known as a “ticker”), you’ll see a description of what this fund is. Verify that this is correct. I’ve done a quick google search on “XAW” and have verified that the “iShares MSCI All Country Index” is the fund I’m looking to buy.

Step 2 – Finding The Market Price of the Investment We Want to Buy (the “Ask” Price)

Click the refresh symbol to the right of the symbol lookup box. This will update the market price data for you.

Underneath the investment symbol information, you will see a few numbers. The only relevant figures are the “Bid” number, and the “Ask” number.

The “Bid” ($26.17 in this example), is the price at which traders currently want to buy this investment. The “Ask” ($26.19 in this example) is the price at which traders want to sell this investment. This is the market pricing for purchasing one share of this index fund.

Since we want to buy this investment now, we need to make an offer which is equal to or greater than the Ask in order for our trade to go through (a.k.a. for our trade to be “filled”).

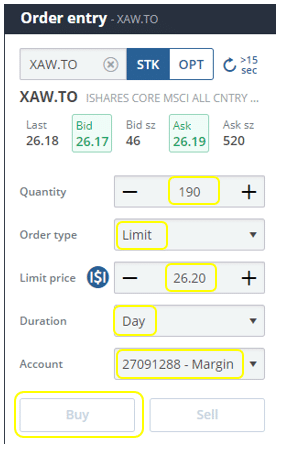

Step 3 – Entering Your Order Details

Now that we know what investment we want to buy and the current market price of that investment, it’s time to submit your trade.

Select the Account that you want to make the trade in

Pick an order type of “Limit” (I’ll explain why down below)

Enter a Limit Price that is one cent above the Ask price that we saw earlier. In this case, this means that we will submit an order to buy at a maximum price of $26.20 (one cent higher than the ask price of $26.19)

Enter the quantity of shares that you want to purchase. To do this, divide the amount of money that you plan to invest by the limit price you’ve entered, and then round down to the nearest whole number. $5,000 divided by $26.20 is 190.84, so I round down to 190 shares.

Choose an order duration of “Day”. This means that your order will automatically cancel if it does not complete today (i.e., if it is not filled today)

After that, click the “Buy” button. Don’t worry! The trade won’t execute now — you’ll have the opportunity to review and finalize your trade in the next step.

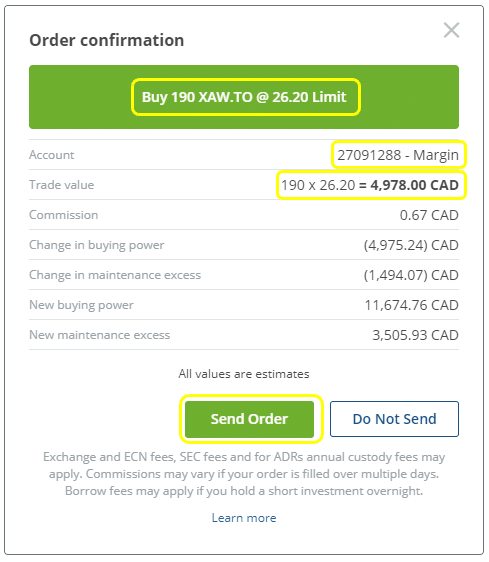

Step 4 – Confirm and Submit Your Trade

After clicking the Buy button, the order confirmation window will pop up.

In the green header bar in the top, you’ll see a summary of the trade that you are making. I am buying 190 shares of XAW, at a limit at $26.20 per share. I do a quick double check — this is correct.

Next, verify that the account info is correct, and that your trade value ($4,978 in this example) is lower than the amount of money that you plan on investing ($5,000 for me, so I am good).

Take a deep breath, read it over one more time, and click “Send Order”.

Congratulations! You’ve submitted your first trade :). I know that this might be stressful and/or might set your heart racing. I promise that it’ll get easier after the second or third time that you go through with making a trade. Just make sure you follow each step, take your time, and verify things before you move on to the next step.

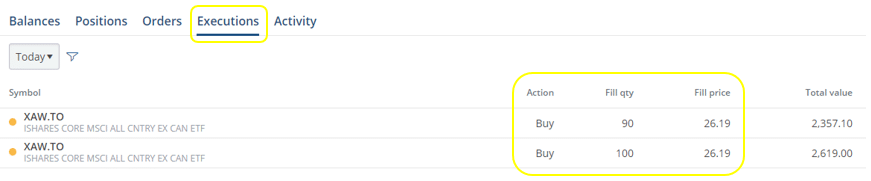

Step 5 – Verify That Your Order Has Been Completed

Last step; all of the heavy lifting is behind you. Now we just need to validate that the order has gone through. Navigate to the “Executions” tab of the page.

In the picture above, you can see that my order for 190 shares of XAW has been executed. Note that my order was completed (filled) at a price of $26.19. This is consistent with the ask price of $26.19 that we saw. Even though I submitted a limit order at $26.20, I still got the best price available. Hurray!

Note: If you don’t see any confirmation here, your trade has likely not been completed yet.

Try navigating to the “orders” tab, where your pending order should be displayed there. It will likely mention that your order has been “submitted”. If so, it is likely that the market price has increased above your limit price, therefore making it possible that your order will not execute today (in which case your order would cancel itself).

If this is the case, try checking back in an hour or two to see if your trade gets filled. You could also cancel your order, refresh the market pricing and try submitting a new trade based on the the refreshed market data.

Why Use a “Limit” Order Type?

In the steps above, I recommended that you submit a “limit” order type.

As some background on this, there are two main order types – “limit” and “market”.

With a limit order, you’re able to specify the maximum price that you’re willing to buy at (or the minimum price that you are willing to sell at, if you are selling shares). This provides protection to ensure that you don’t end up buying shares at a significantly different price than you were expecting. In the example above, I specified that I did not want to buy at a price exceeding $26.20 per share.

On the other hand, a market order means that you are willing to buy at the best available price currently. Essentially, you agree to take the lowest price at that moment, regardless of what it is. Share prices can be volatile, so I don’t recommend using a market order because this can lead to some bad surprises. For example, while you are submitting your trade, the fund’s market price could increase by $1 per share, and you’d be committing to buy at that elevated price.

Keep it simple and use a “limit” order.

Why Set a Limit Price that is Higher than the Ask Price?

Now you might be asking: shouldn’t I input a limit price that is lower than the ask price, as opposed to a price higher than the ask price?

This may seem logical given that you’d “save” a cent or two on the price that you buy your shares at, but this actually creates a new risk. If the current ask price is $26.19, and you say to the market that you don’t want to purchase shares unless the price falls to $26.17 (two cents lower), your order may never go through. You are effectively saying that you won’t buy unless the market price goes down.

This is “penny wise, pound foolish”. For the opportunity to score a minuscule win (a discount of a couple cents per share), you risk that your trade doesn’t go through, meaning that you’ll miss out on investment gains. Since the market tends to go up in the long run, delaying your entry into the market only hurts you.

What Time Should You Trade At?

The main stock exchanges in Canada & the US are open between 9:30AM until 4PM on Monday to Friday (except for holidays).

As much as possible, you should submit trades during market hours. This means that you’ll need to submit your trades during the work day.

While it is possible to submit trades outside of market hours (known as pre-market trading or after-hours trading), you increase the chance that your order doesn’t go through if you do this.

Companies tend to release big news outside of market hours (before or after the trading day). As such, when this happens the prices can open at a much different value than what the previous day’s closing price was.

Because of this, if you submit a limit order based on the previous day’s closing price, your order might not go through and you will have to re-submit. Each day that you’re out of the market means that you miss out on potential investment gains.

The bottom line is that you should try to submit trades during market hours (9:30AM to 4PM on weekdays) if you can.

Takeaways: How to Trade Online

Let’s put it all together. Once you learn how to trade online and get some practice with it, purchasing investments becomes a simple recipe. Follow these five steps:

Look up the correct investment symbol

Find the current market price of the investment you want to buy (the ask price)

Enter your order details (remember to use a limit order type at a price that is one cent above the ask price)

Confirm and submit your trade

Verify that your order has been completed

Your Assignment

Log in to your online brokerage account and take note of the total amount of money you plan on investing

Divide up that total amount of investment money into the different individual investments you want to make. This should be based on your chosen asset allocation (which we discussed in the previous lesson). For example, if you have $5,000 and plan to invest 60% in fund A, 30% in fund B, and 10% in fund C, you would allocate:

$3,000 towards fund A

$1,500 towards fund B

$500 towards fund C

Follow the guide above to execute each of the trades you plan to make

Once you’ve verified that your trades have gone through, record each of the trades that you’ve made (investment fund name, # of shares, price per share, total $ value). I’ve built a spreadsheet that you can use to track your investment portfolio. This sheet has a template for you to enter your trade details, automatically pulls today’s market price data from Google Finance to show what your portfolio looks like, calculates portfolio performance metrics, and will help you automate your re-balancing calculations as well

If you’d like to open a Questrade DIY (Do it Yourself) account for low-cost index investing, please feel free to add my referral code of 336413903418268 when you open the account. We will both receive $50 in that case!

Disclaimer: This information is provided for illustrative and educational purposes only. Your situation is unique, and I do not guarantee the results or the applicability of this information to your situation.

None of this information should be considered investment advice or a recommendation to buy or sell individual securities.

Readers should do their own research before making any financial or investment decisions.

Moonshine Money: A Do-It-Yourself Guide to Personal Finance

Building wealth relies on a simple recipe: you need to spend less than you make, invest the difference wisely, and have a healthy dose of patience. No more and no less.

You don’t need to be a six-figure earner, have a trust fund, or be a stock-picking wizard.

At first, investing can seem like a big and scary topic. You might be tempted to rely on professional advisers (a.k.a slick salespeople in suits) to handle your money for you. If you go down that path, you’ll end up paying out a sizable chunk (10-50%) of your net worth in fees to your advisers. This means that you’ll have to work many more years to meet your financial goals, or that you’ll simply never get there.

It doesn’t have to be this way. By using a tried and true do-it-yourself investing strategy, you’ll be in full control of your money and will save hundreds of thousands of dollars in investment fees over the long term. No Ivy-league education required.

In Warren Buffett’s words:

“Success in investing doesn’t correlate with I.Q. once you’re above the level of 25. Once you have ordinary intelligence, what you need is the temperament to control the urges that get other people into trouble in investing.”

Implementing a successful do-it-yourself investing strategy comes down to a few simple steps:

Invest in stocks, with a splash of bonds

Use a low-cost, diversified, and passive investing strategy

Take advantage of tax-sheltered accounts

Stay invested

Re-balance your portfolio when necessary

Invest in Stocks, With a Splash of Bonds

Think of your investment portfolio as a cocktail (however for best results, keep investing and drinking separate). Your beverage should be heavy on stocks, with a light amount of bonds mixed in.

Stocks are the fuel of your wealth building efforts. Throughout modern economic history, owning a broadly diversified basket of stocks has consistently brought about tremendous increases in wealth.

Bonds add stability to your portfolio. The performance of stocks and bonds tend to be out of sync. When stocks do poorly, bonds often stay flat or even increase in value.

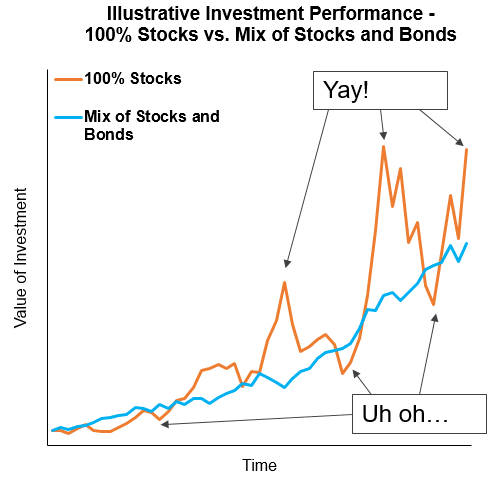

Investing in bonds allows you to smooth out the ride. Consider that the U.S. stock market has had multiple occasions in which it lost 20 to 40% of its value in a single year. As your investment horizon becomes shorter (as you near retirement or near a withdrawal from your portfolio) you should shift from stocks to bonds in order to protect your wealth.

Think of stocks as a wealth builder and bonds as a wealth preserver. As you increase your allocation in stocks, you increase your long term expected investment returns, but you also increase the chances that you’ll suffer big losses in the short term.

The gist: most people should have 60-90% of their investment portfolio in stocks, with the remainder invested in bonds. The longer your investment horizon and/or the higher your risk tolerance, the more stocks you should own.

Use a Low-Cost, Diversified, and Passive Investing Strategy

So, which stocks and bonds should you buy? Maybe a few shares of Apple; how about Tesla?

The short answer: you should buy ALL of the investments.

The longer answer: you should be investing in Exchange Traded Funds (ETFs for short).

An ETF is an investment that tracks the performance of a large number of individual investments.

For example, you may have heard of something called the S&P 500 index. This “index” tracks the performance of the 500 largest American companies (including Apple, Google, Microsoft, GE, Walmart, Proctor and Gamble, so on and so forth).