Building wealth relies on a simple recipe: you need to spend less than you make, invest the difference wisely, and have a healthy dose of patience. No more and no less.

You don’t need to be a six-figure earner, have a trust fund, or be a stock-picking wizard.

At first, investing can seem like a big and scary topic. You might be tempted to rely on professional advisers (a.k.a slick salespeople in suits) to handle your money for you. If you go down that path, you’ll end up paying out a sizable chunk (10-50%) of your net worth in fees to your advisers. This means that you’ll have to work many more years to meet your financial goals, or that you’ll simply never get there.

It doesn’t have to be this way. By using a tried and true do-it-yourself investing strategy, you’ll be in full control of your money and will save hundreds of thousands of dollars in investment fees over the long term. No Ivy-league education required.

In Warren Buffett’s words:

Implementing a successful do-it-yourself investing strategy comes down to a few simple steps:

- Invest in stocks, with a splash of bonds

- Use a low-cost, diversified, and passive investing strategy

- Take advantage of tax-sheltered accounts

- Stay invested

- Re-balance your portfolio when necessary

Invest in Stocks, With a Splash of Bonds

Think of your investment portfolio as a cocktail (however for best results, keep investing and drinking separate). Your beverage should be heavy on stocks, with a light amount of bonds mixed in.

Stocks are the fuel of your wealth building efforts. Throughout modern economic history, owning a broadly diversified basket of stocks has consistently brought about tremendous increases in wealth.

The U.S. stock market has returned an average of nearly 7% per year in inflation-adjusted investment returns. This means that on average, your money would double every 10 years.

Bonds add stability to your portfolio. The performance of stocks and bonds tend to be out of sync. When stocks do poorly, bonds often stay flat or even increase in value.

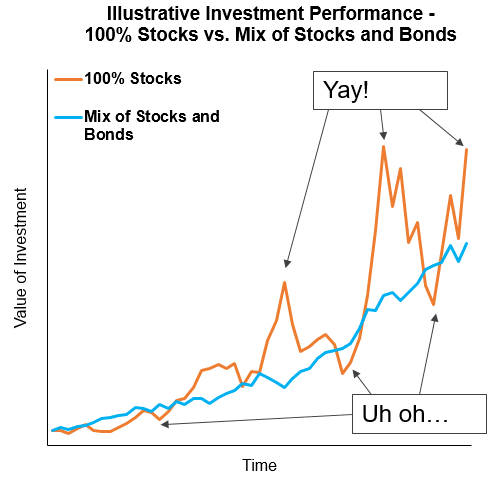

Investing in bonds allows you to smooth out the ride. Consider that the U.S. stock market has had multiple occasions in which it lost 20 to 40% of its value in a single year. As your investment horizon becomes shorter (as you near retirement or near a withdrawal from your portfolio) you should shift from stocks to bonds in order to protect your wealth.

Think of stocks as a wealth builder and bonds as a wealth preserver. As you increase your allocation in stocks, you increase your long term expected investment returns, but you also increase the chances that you’ll suffer big losses in the short term.

The gist: most people should have 60-90% of their investment portfolio in stocks, with the remainder invested in bonds. The longer your investment horizon and/or the higher your risk tolerance, the more stocks you should own.

Use a Low-Cost, Diversified, and Passive Investing Strategy

So, which stocks and bonds should you buy? Maybe a few shares of Apple; how about Tesla?

The short answer: you should buy ALL of the investments.

The longer answer: you should be investing in Exchange Traded Funds (ETFs for short).

An ETF is an investment that tracks the performance of a large number of individual investments.

For example, you may have heard of something called the S&P 500 index. This “index” tracks the performance of the 500 largest American companies (including Apple, Google, Microsoft, GE, Walmart, Proctor and Gamble, so on and so forth).

You can purchase ETFs that track the performance of the overall S&P 500 index. This means that you essentially own a small slice of every one of the 500 largest companies in the U.S.

Note: People often use the term ETF interchangeably with the term “index fund”.

There are a huge variety of ETFs that you can purchase: American stocks, Canadian stocks, emerging markets stocks, technology stocks, and all of the above but for bonds instead.

Why invest in ETFs?

- Diversification: By investing in ETFs, your investment will spread across hundreds or thousands of different companies. These companies will be in different industries (technology, healthcare, mining, etc.) and will also be in many different countries. Contrast this to investing in just a handful of individual companies — if one of those companies goes bankrupt, your investments will be sunk

- Simplicity: If you wanted to replicate the diversification of an ETF on your own, you’d need to manually make investments in thousands of companies. This would require a mind-boggling amount of work

- Low fees: When you invest in an ETF, you will pay an annual “management fee”. This is paid to the company that creates and manages the ETF to compensate them for executing the trades, re-balancing the allocation, admin and paperwork. ETFs have extremely low fees. For example, Vanguard offers an S&P 500 index fund (symbol is VOO) which charges 0.04% per year. If you had $10,000 invested in this fund, this would come out to a fee of $4 per year. As we’ll see below, people invested in actively-managed mutual funds are paying significantly higher fees

The goal is to use a low-cost, diversified, and passive investing strategy. This is often known as a “couch potato” strategy. With some work upfront and a bit of tracking and maintenance each year, you’ll be able to lean back and watch your investments grow.

In contrast with the recommended couch potato strategy, the vast majority of people are using an “actively-managed mutual fund” strategy for their investing.

Even if you’re never heard the term actively-managed mutual fund, there’s a good chance that you are already using this strategy.

The reason is that every major bank pushes their customers towards this path. It usually goes like this: you ask someone at your bank for help with making an investment plan, you meet with a financial adviser at the bank, and then you’re persuaded to invest in mutual funds.

What exactly is an actively-managed mutual fund?

This refers to investment funds which are run by a manager who is trying to pick hot stocks and time the market, with the end goal of outperforming the average market return.

It sounds pretty great in theory.

However, time and time again this has been shown to be a losing strategy. Over long periods of time (10+ years), more than 90% of actively managed mutual funds have lower investment returns compared to a simple couch potato strategy. See these S&P reports by country for more detail if you wish.

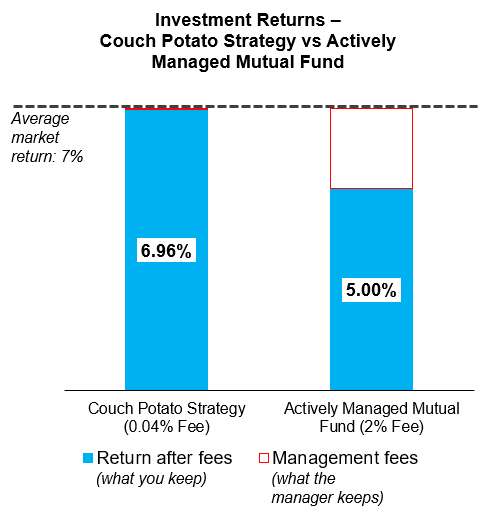

How is this possible? How can Ivy-league educated fund managers do worse than a simple strategy that you and I can implement? The answer lies in the extremely expensive fees that these managers charge.

Before fees are taken into account, these managers tend to have performance which matches the overall market. However, after their fees are taken out, the returns for actively-managed mutual funds significantly lag behind the overall market.

Think of these fees as being what the manager pockets, and the return after fees as being what you keep. By minimizing your fees, you end up with higher returns.

The impact of minimizing management fees can be massive when this occurs over a long period of time.

Take the example of a 25 year old who saves $5,000 per year for 40 years. By using a couch potato strategy and earning a return of 7% per year, they’d end up with ~$1M by age 65. If instead they invest their money in actively-managed mutual funds and only earn 5% per year after fees, they’d have ~$600k (see the result visualized here). $400k (four hundred thousand dollars!!) has been eaten up by fees.

I repeat — using a low-cost, diversified, and passive investing strategy (a.k.a. couch potato strategy) can save you hundreds of thousands of dollars. Spending a few hours learning how to implement this strategy will be well worth it.

Let’s take a look at some real examples.

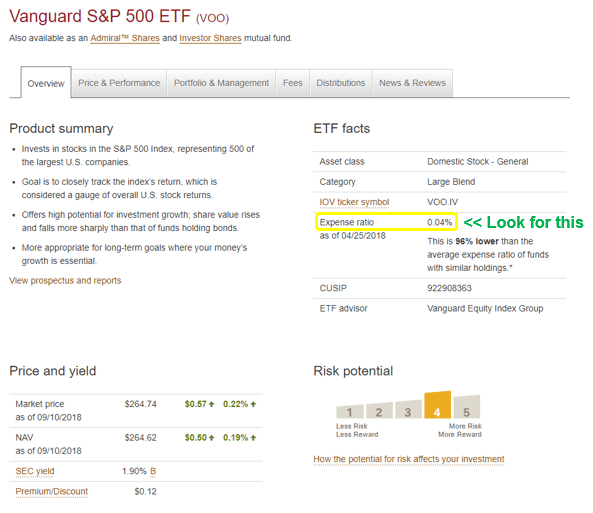

The picture below is showing the Vanguard VOO ETF which we discussed before. This ETF tracks the S&P 500 index. The “expense ratio” is only 0.04% per year ($4 per year on an investment of $10,000).

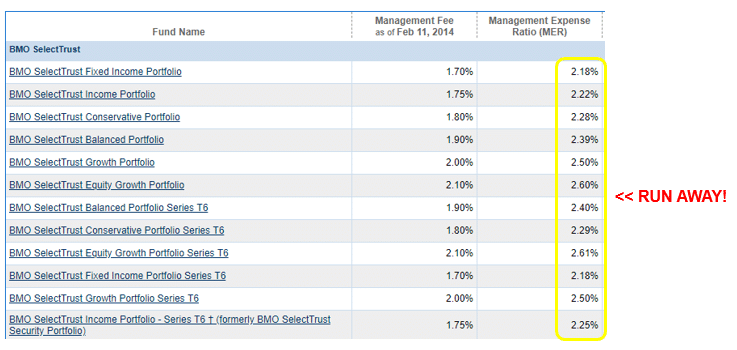

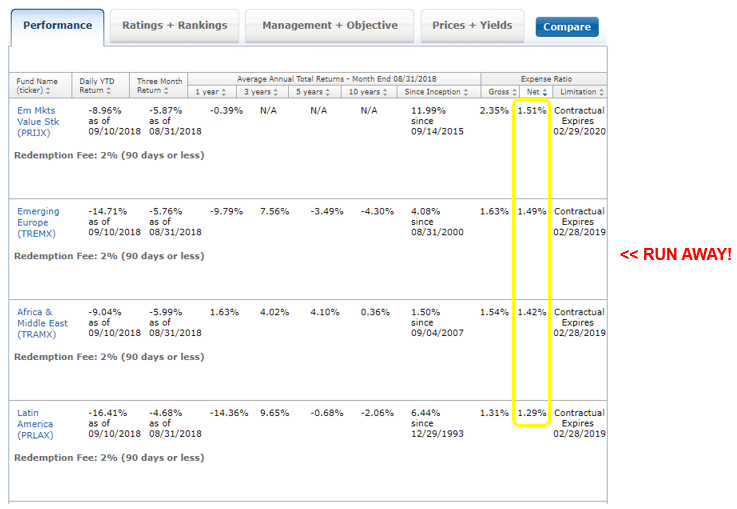

Now compare this against some actively managed mutual funds from BMO (a major Canadian bank). The management fees for these funds are over 2% per year — more than 50 times higher than the S&P 500 ETF.

And below, the management fees for mutual funds from T. Rowe Price (a large American investment manager). Better than BMO, but still terrible when compared against a low-cost ETF.

If you still aren’t convinced that you should avoid actively-managed mutual funds like the plague, read through this article from the Financial Times. A few telling excerpts:

If the managers themselves doesn’t trust in their ability to beat the market, should you?

You can say “conflict of interest” and “hypocrisy” one more time.

What about robo advisors? For those who haven’t come across them, robo advisors are companies that typically implement a couch potato investing strategy on your behalf (similar to what is discussed here), and charge you for their services — typically a fee of 0.5% on top of the management fees charged by the underlying ETFs.

If you’ve gotten this far, I see no reason to invest your money with a robo advisor or similar type of service. By retirement age, over 10% of your portfolio would be eaten up by these additional and unnecessary fees.

The gist: Forget about actively-managed mutual funds and robo advisors. Follow a couch potato investing strategy using ETFs (low-cost, diversified, and passive investing strategy).

Take Advantage of Tax-Sheltered Accounts

As shown above, you can maximize your investment returns by minimizing your investment fees. The same goes for taxes on your investment portfolio — the less taxes you pay on your investments, the larger your investments will grow.

Before discussing the details of the “tax-sheltered” accounts that we can use to reduce taxes, it’s a good time to talk about the concept of what we’re trying to do here.

The standard cycle of investing money goes like this: you save a portion of your paycheck, invest that money, let it grow over time, and then sell your investments to fund your lifestyle once you stop working. If you follow this cycle, you will pay two types of taxes — income taxes owed on your initial paycheck, and the capital gains taxes owed on the profits that you’ve made on your investments when you sell them.

Income taxes are the taxes that are automatically deducted from your regular paycheck (as discussed in a previous lesson).

Capital gains taxes are amounts that you owe on the profits made on your investments. For example, if you invest $1,000, let it grow for 20 years until it reaches $3,000, and then sell your investment (i.e., turn it back into cash), you would have made a profit (a.k.a. capital gain) of $2,000. You will need to report your $2,000 capital gain on your tax return and pay taxes on that amount.

Even though you paid income taxes on your initial paycheck, you still owe a second round of taxes when you make investment returns with money. Not super fun.

When all hope seems lost… have no fear, tax-sheltered accounts are here!

Tax-sheltered accounts are available to all Canadians and Americans (and citizens of many other countries not discussed here). By moving your money into these accounts, and then purchasing your investments within these accounts, effectively you’ll no longer pay capital gain taxes on your investments.

Canadian Tax-Sheltered Accounts

The main tax-sheltered investment accounts for Canadians are the Tax-Free Savings Account (TFSA) and the Registered Retirement Saving Plan (RRSP).

For a good overview of what these accounts are and how they differ, read through these articles:

- Ratehub’s introduction to the TFSA and RRSP accounts

- The Wealthy Barber explains: TFSA or RRSP?

- Retire Happy: When should you not use an RRSP?

My over-simplified take on this: if you are unsure of what to do, as a default you should start with putting your money in a TFSA. It is the more flexible option, and the money can be transferred into an RRSP at a later date (but not vice versa).

American Tax-Sheltered Accounts

The major tax-sheltered investment accounts that Americans have access to are Roth accounts and Traditional accounts.

To understand what these are, read through:

- CNN Money’s ultimate guide to retirement

- Winning Personal Finance’s comprehensive guide on Roth IRAs vs Traditional IRAs

If you’re in the fortunate position to be able to max out all of your tax-sheltered accounts, please do so. If you still have money left over, you should invest your money in a regular taxable account (a.k.a cash account / non-registered account). Keep in mind that you’ll have to pay capital gains taxes on your investment profits in this account.

However, most people will need to make a choice between investing in one account or the other. Do not get stuck in analysis paralysis. Investing in a tax-sheltered account is always better than investing in a regular taxable account, and is infinitely better than choosing to not invest at all.

As a final note, make sure you understand that a tax-sheltered account is not an investment in and of itself. You can’t just move your money into the account and expect it to grow over time. A tax-sheltered investment account is just the container in which you hold your investments. After you contribute money into the account, make sure that you use that money to purchase the ETFs / index funds that you want.

The gist: Take advantage of tax-sheltered accounts as much as possible. Move your savings into these accounts, and then purchase your ETFs with the money that you’ve contributed. This allows you to reduce your taxes owed on your investments, thereby increasing your investment returns. Don’t get too hung up on making the “perfect” choice of account to use — not taking any action will always be the more costly choice.

Stay Invested

So-called financial “experts” like economists, traders, and fund managers are famously poor at predicting when a recession will happen. A popular dig at these gurus goes:

The next time you hear some famous and well-credentialed individual going on about how the market is likely to crash in the next year, keep in mind that reputable people are ALWAYS going on about how a crash is right around the corner.

Take a look at this great chart on the S&P 500 versus market pundits. If you would have listened to these experts and sold your investments, you’d have missed out on the stock market more than doubling in value from 2012 to 2018.

Market experts are constantly crying wolf.

Instead of being afraid of short-term volatility in the market, you should be concerned about pulling out of the market and missing out on investment returns. An analysis from JP Morgan / Business Insider shows how your annual returns are significantly impacted if you miss the best trading days.

From 1994 to 2013, the overall return of the S&P 500 was ~9.2% per year. If you would have missed just the best 10 trading days (out of 5000 total days — or 0.2% of the total days), your return would drop to 5.4%. Missing just a tiny fraction of the overall trading period would have tanked your investment returns.

The point being: if you try to jump in and out of the market you are very likely to miss out on the small amount of days that make up most of your returns. I repeat — time in the market is more important than timing the market.

Don’t listen to CNBC, don’t follow the predictions of the latest “stock market guru”, just don’t.

Frankly, no one knows what the stock market will do in the short term. These types are predictions are just noise that aren’t worth the paper they’re printed on.

As always, Warren Buffett puts it best:

As a testament to the power of patience, check out the amazing story of Leonard Gigowski, a former cook in the navy, meat cutter, and eventual owner of a corner grocery store, who quietly amassed a fortune through his life. When he passed away, he donated $13M to his alma mater.

The gist: Think of your investment portfolio as a bar of soap; the more you touch it, the less you have. Set it and forget it.

Re-Balancing Your Portfolio

When you make your first round of investments, your asset allocation will be done in clean & round percentages — for example, 80% of your money in stocks and 20% in bonds.

As time passes, your asset allocation may get a bit out of whack if the performance of your stock and bond investments haven’t been the same. You might find that your stock allocation has dropped to 73% or increased to 86%.

When your allocation drifts far away from what you’d like it to be, this is the time to re-balance your portfolio.

There are two ways of doing this:

- Sell some of one investment, and use the proceeds to buy some of the other investment. If your stocks have done much better than your bonds, this would mean selling some shares of your stock fund and using the money to invest in your bond fund

- Use new money that you are investing to re-balance your portfolio back to your target weightings. This is the method that I always use. Since I’m in the midst of my career and am able to invest a good chunk of new money into the markets each year, I just use that new money to re-balance as appropriate

How often should you re-balance?

There’s no hard science to guide us here. To find the optimal re-balancing frequency, you’d need to know how markets will perform in the future (not doable without a crystal ball).

I review my investment weightings once or twice a year, and re-balance if my weightings are significantly out of step. I’m currently invested in 90% stocks and 10% bonds, and will re-balance if my bond percentage gets below 7% or above 13%. Again, no magic here.

The gist: Your asset allocation can and will get out of whack from time to time. When that happens, re-balance your portfolio with new money or by selling one investment and buying another. Don’t get too fussed about this, an annual check up is absolutely fine.

Assignment #1 – Open An Investment Brokerage Account

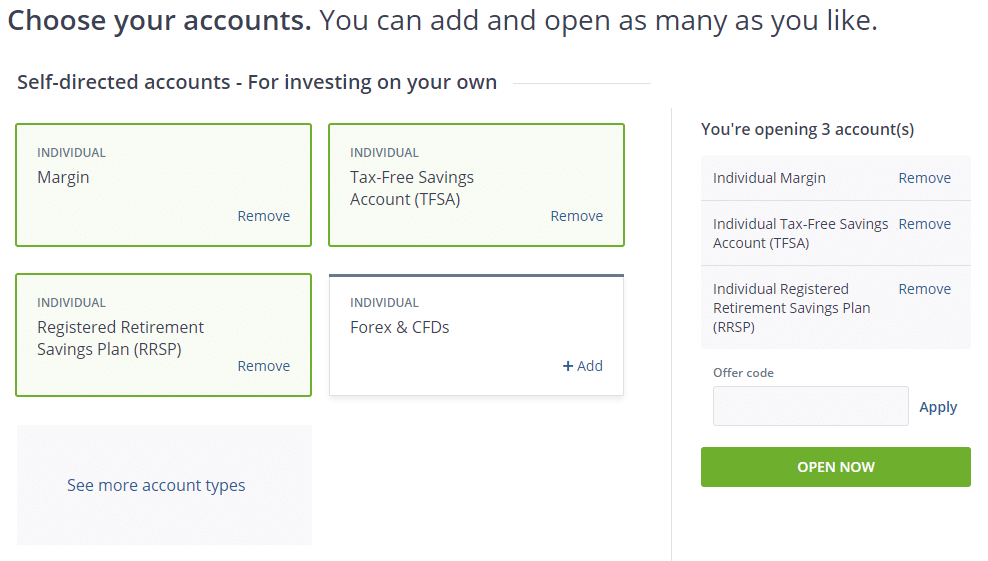

Open an account with your investment brokerage of choice. Make sure that you apply to open tax-sheltered accounts.

Canadian brokerages: Questrade is the best option out there. There are no fees to open an account, and it’s free to buy ETFs through Questrade (versus $10 per trade at the major banks). Selling ETFs will cost you $5 to $10 per trade.

Open a “self-directed” account (not a “managed investing” account). When applying, you can open up a margin account (a.k.a regular taxable account), a TFSA, and an RRSP account all at the same time.

American brokerages: Vanguard is simply the best out there. Schwab and Fidelity are also good options.

Assignment #2 – Decide On Which Investment Funds You’ll Own

Decide on the index funds that you want to buy in your portfolio. Keep it simple! For the vast majority of people, just one, two, or three funds at most will do the job.

Portfolio guides for Canadians: I recommend that you follow the approach from Canadian Couch Potato. I’ve been managing my own investments according to this guide for several years now.

Portfolio guides for Americans: The Boglehead Lazy Portfolio guide has some good recommendations.

Take your time to get acquainted with the potential options. I know that the sheer volume of acronyms can be intimidating in this part. Please don’t let this hold you back.

Keep it simple: a portfolio that is mainly weighted towards stocks (60 to 90%) with the remainder being invested in bonds will serve you well for decades to come.

For some guidelines on how to pick your asset allocation (% in stocks and % in bonds), read through this article from CCP. The key factors to keep in mind are your investment horizon, risk tolerance, and your need to take risk.

Remember that a higher allocation towards stocks will yield both higher returns (upside) and higher risk (downside). As you get older, your asset allocation should change to become more conservative (i.e., more bonds).

Next steps

Now that you’ve opened up your investment accounts, and have decided on your portfolio asset allocation (what funds you will buy and in what %), the last step is to actually log in to your online brokerage account to purchase your investments.

In the next lesson, we’ll go through a detailed how-to guide on everything you need to do to make your first trades online.

Disclaimer: This information is provided for illustrative and educational purposes only. Your situation is unique, and I do not guarantee the results or the applicability of this information to your situation.

None of this information should be considered investment advice or a recommendation to buy or sell individual securities.

Readers should do their own research before making any financial or investment decisions.

This information is presented in a very clear & logical manner. I appreciate how easy it is to understand and how well you have broken down the material!

Thanks Rachel, glad to hear it and very nice of you to let me know!

The recommendation for Canadian Couch Potato Model Portfolios is a great one!

I think the link is broken, you can link to the main model portfolio section https://canadiancouchpotato.com/model-portfolios/

or choose a portfolio from there!

I know its hard to keep every link up to date, especially with the tons of great resources that you have and always more coming,

Really enjoy an appreciate this content that your providing and this will continue to be a resource I share with others!

Thank you Kajendra! For spotting that broken link, suggesting a new one, for the kind words, and for sharing my site with others 🙂

I’ve replaced the link (with the one you mentioned).

Cheers!

Amazing content. I struggled to explain personal finance to my friend who recently graduated and got his first job. I am by no means a guru so explaining from A to Z is a long process. I think I will direct him here and he can read great content on here himself! Thank you and appreciate the hard work you put into this!

Thanks Nicholas, happy to hear that 🙂

Helping new graduates and other people who are getting started with personal finance is precisely who this guide was written for.

It’d be great if you could share.

Thank you very much for your insight.

Quick question – My company does an RRSP match and we only have mutual fund or GIC as options. What should I be doing, I contribute the minimum required to get the match of 3%, have now moved and invested in a S&P500 tracking MF and MER is (0,18%). Please suggest what we should do in such situations

Hi KK,

Contributing the minimum required to get the full company match makes sense. I also prefer to contribute the minimum to get the “free money” matching, and then invest the remainder by myself.

Investing in a S&P500 tracking mutual fund also makes sense. 0.18% is a decent annual management fee.

I’d just recommend that you assess what you’re target asset allocation should be (stock vs. bond mix), and then use your own personal funds to reach that target allocation.

All in all, seems like you’re doing a good job. Keep it up!

Fantastic article! I noticed a small typo: “manger” instead of “manager.” Running it through Grammarly might help catch these.

Switching from actively managed mutual funds could save my partner a million in the long run.

Thank you! I’ve fixed it.

I wish I’d read this before creating my own portfolio. I ended up realizing that using just two or three index funds would have returned the same results as the actively managed funds, just like you point out in your article. I’ll be sure to share this with friends who are also trying to figure out how to invest. Thank you!

Thank you Steve — the feedback is appreciated. Also many thanks for sharing this with friends. Cheers 🙂

Questrade is no longer charging their $4.95 to $9.99 fee to sell ETF units (presumably due to the “wealthsimple effect”).

Suggest updating this article accordingly.