With a bit of knowledge, a solid plan, and a heavy dose of hard work, you can become debt-free.

Read on for a tried and true method for getting your money to work for you instead of against you.

Get Organized

Earlier in this course, you made a list of all your financial accounts and their current balances. Let’s refer back to that list, taking a look specifically at the debts section. We’ll need to add in a bit more information.

For each of your debts (credit card, student loans, car loans, mortgage, personal loans, etc.), make note of the current balance, the interest rate, and the minimum payment. Feel free to add in this information in a new tab of your spreadsheet, or stick with a pen and paper if you prefer.

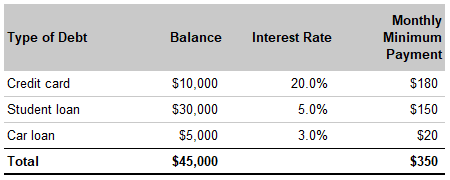

To illustrate, let’s assume that I owe $45,000 in total debt split between a credit card, a student loan, and a car loan. I’ve also listed out the interest rate and minimum payments for each of these debts.

Minimum Payments

No matter what, you need to find a way to make the minimum payments on ALL of your debts.

If you start to miss the minimum payments on any of your debts, there will be significant negative consequences. Depending on the type of debt and the provider, you could face late fees, increased interest rates, and/or repossession of your belongings.

Before thinking about making any non-essential purchases or doing any kind of investing, make sure that you have the cash to pay all of your monthly minimum payments first.

For my example, between my three types of debt I’ll need to make minimum payments of $350 per month.

Your Current Trajectory

Let’s take a step back and assess the situation.

You’ve gotten organized with a list of your debts and the relevant info for each. You might be asking — So what does this all mean? How quickly will I be able to get out of debt? How much interest will I pay?

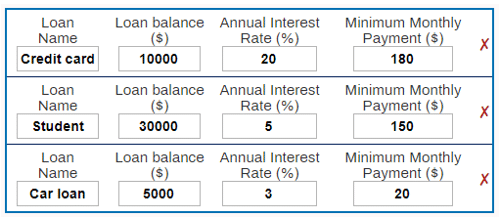

I’ve built a Debt Payoff Planner to help answer these very questions. Open it up, and input each of your debts into the tool. The list that we made previously contains all of the inputs you’ll need for the tool.

Once you’ve added in all of your loans, the tool will show you the date at which you’ll be debt free, and the total amount of interest that you’ll pay.

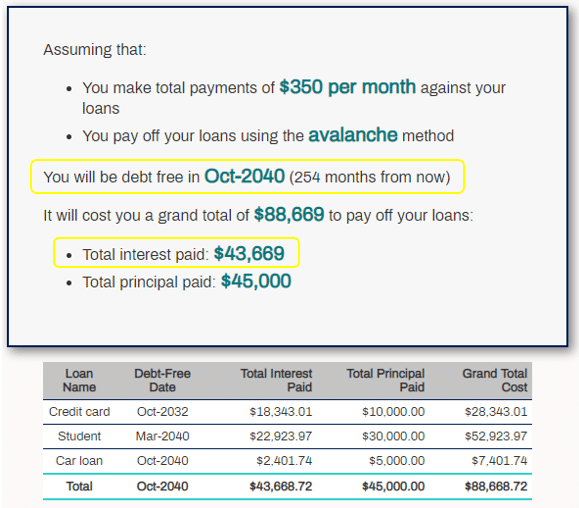

In my hypothetical example, if I only make the minimum payments on my debts ($350 per month), I’ll be debt-free in 254 months (over twenty years from now!), and will have paid over $43,000 in interest on that debt. Ouch.

Make note of what these numbers are for your own scenario. It’s not pretty, but it is what it is. Ignoring the truth won’t make it go away. By crafting a plan and seeing it through to the end, you can and will become debt-free faster.

Finding Extra Room Within Your Budget

The minimum payments on your debts should absolutely be treated as MINIMUM payments. The only way to beat the timeline that we saw above is to put more money towards your debts.

In the previous lesson on budgeting, you gathered information on your historical spending habits. Take another look at that, and try to split up your spending between “essential items” (such as rent, groceries, utilities, transportation) and “discretionary items” (eating out, travel, entertainment, gifts, etc.).

Which of the discretionary items can you cut back on to make more room for paying off your debts?

What would a “bare bones” budget look like? Can you try to live on that reduced budget for a few months?

I won’t pretend that this is a simple task, but doing this will significantly accelerate your progress towards a debt-free future.

Designing a Debt Reduction Plan

Once you’ve freed up some extra cash flow to put towards your debts, you’ll need a plan for how you allocate that money. Should it go towards credit cards first, or how about my student loans?

There are two schools of thought about how to approach this problem: the avalanche method and the snowball method.

The avalanche method tells us to put all the extra cash flow towards the debt which has the highest interest rate. In my case that would be the credit card at 20% interest. I would increase my monthly payment on my credit card, while only making the minimum payments on my other debts.

The avalanche method is the optimal solution from a mathematical perspective. This method allows you to pay the least amount of interest, and makes you debt-free as fast as possible.

If that’s the case, shouldn’t everyone use the avalanche method? Not so fast.

While the avalanche method is best from a pure numbers perspective, it ignores the emotional and mental challenges of becoming debt-free. This is where the snowball method comes in.

The snowball method tells you to ignore the interest rates on your debt. Instead, you funnel all of your extra cash flow towards the loan with the lowest balance remaining. This means that I would put my extra cash towards my car loan (with a balance of $5,000 remaining). After the car loan is paid off, I’ll move to the credit card (second smallest debt), and then finally the student loans (my largest debt outstanding).

This method is not optimal from a pure financial perspective. However, for many people this is the best way to proceed. By focusing on the smallest debt that you have, you rack up quick wins, which helps to keep you motivated to get on with the next challenge.

Research from the Harvard Business Review suggests that the snowball method (paying the smallest debts first) is the most effective strategy, even though it is not mathematically optimal.

If you’re worried about losing momentum midway through your plan, consider using the snowball method.

Enough talk, how does this apply to your situation?

Head back to the Debt Payoff tool that we were just using. It allows you to set your monthly payments at whatever level you choose, and lets you use either the avalanche or snowball methods to allocate any extra money you’re throwing towards your debt (in excess of the minimum payments).

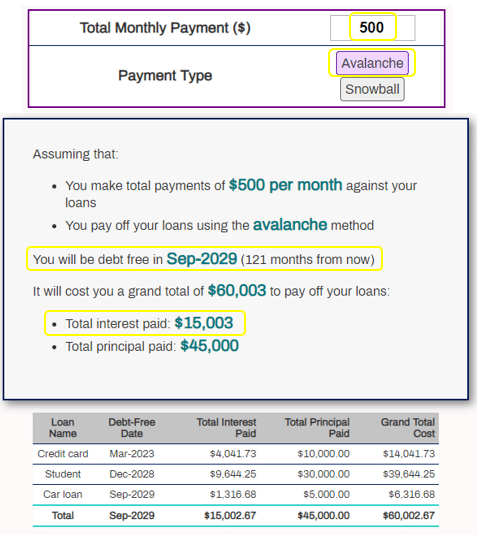

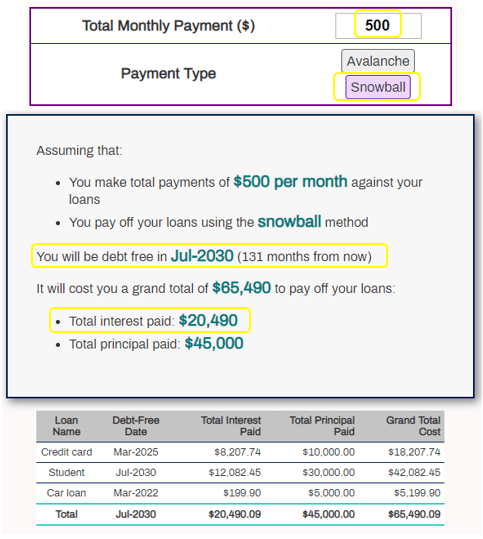

Let’s see what it looks like if I increase my monthly payments by $150 (from $350 to $500), and use the avalanche method.

I’d be debt free in 121 months (instead of 254 months), and would pay total interest of $15,000 (instead of $43,000). As you can see, even small lifestyle changes can make a HUGE difference.

And for comparison’s sake, here are the results for the snowball method.

I’d be debt free in 131 months (10 months later versus the avalanche method), and would pay $20,500 in interest (~$5,500 more interest versus the avalanche method).

Personal finance is just that — personal. Choose the path that makes you feel more comfortable. In the end, as long as you’ve put in the effort to free up extra cash to pay back your debts, you’re well on your way to being debt-free :).

Good Debts and Bad Debts

Becoming debt-free is a huge milestone that will provide you with peace of mind.

However, in some situations it may be a better financial decision to put your extra cash flow towards making investments, rather than continuing to pay off your debts.

For example, if you have debt at a 3% interest rate, but would be able to invest your money and earn a 7% return, from a financial perspective you’d be better off investing your money rather than using it to pay off debt.

For some context, investments in the overall stock market tend to earn a return of 5% to 10% per year. If you’re new to investing, don’t worry — in the next chapter we’ll cover everything you need to know about the topic of investing.

As a general rule of thumb, you may want to consider taking your time in paying off debts that have an interest rate of ~5% or less. Debt which has a relatively low interest rate can be considered “good debt”. For many people, their mortgage may fall into the “good debt” category.

There are two very important caveats if you are considering this strategy: (1) any money that you don’t use for paying back this debt needs to be put towards making investments, and (2) you still need to make the minimum payments on that debt.

If you are looking to maximize your net worth, you may want to consider paying off all of your “bad debts” (debt with an interest rate of 5%+) as soon as possible, but take your time to pay off your good debts. This way, your cash would be invested at a higher return, making you wealthier in the long-run.

If being debt-free as soon as possible will help you to sleep at night, feel free to disregard this discussion entirely. Personally, I try to avoid debt as much as possible. I’ll gladly give up some potential investment returns in order to eliminate my debts entirely.

Again, this is a choice for you to make.

Staying Debt-Free

Now that you’ve dug yourself out of a hole, whatever you do, don’t get back in.

Always pay off your credit card balance in full, each and every month. If you can’t do that, you simply shouldn’t have spent the money that you did. If having a credit card tempts you to make purchases you can’t afford, consider getting rid of your credit cards altogether. Stick to cash and debit cards.

Stop financing your purchases. Don’t finance your new couch. Don’t finance your next car. And forget about the new iPhone.

Stay within your budget. In the previous lesson you created a budget and were tasked with reviewing and updating that budget on a monthly basis. If you want to stay out of debt, there can’t be any cheat months. Each month needs to be planned so that your cash inflows are greater than your cash outflows. Budget regularly, and stick to that plan.

Conclusion

Follow these steps to become debt-free:

- Get organized: Make a list of your debts, including their current balances, interest rates, and minimum payments

- Assess the damage: Use this Debt Payoff Planner to find out when you’ll be out of debt, and how much interest you’ll pay

- Adjust your budget: Come up with some extra cash to put towards your debts

- Design a debt reduction plan: Use either the avalanche method or the snowball method. Your choice

- Stay debt-free: Pay off your entire credit card bill, every month. Stay within your budget. No cheating

On this topic I have a question.

Let’s say a person has got themselves into a bad situation and has ignored their debts for some years. They have had no assets or income for a significant period of time. Many of these debts are now interest frozen, with minimum payments that are negotiable and in many cases settlement offers that are lower than the outstanding balance.

Now this person has found a regular income and wants to resolve the situation.

In this scenario, should that person channel more funds into those debts that are no longer attracting interest or fees, or should they instead invest their money in savings accounts and other investment avenues?